Green Bonds: The Shape of Green Fixed-Income Investing to Come

2,262

Fixed-income securities that use their proceeds toward the financing of ESG-aligned projects have proven particularly attractive among investors. Their volume has been increasing exponentially since…

Dr. Kim Schumacher

Lecturer in Sustainable Finance and ESG at the Tokyo Institute of Technology

Abstract

This paper serves as an introduction to the Journal of Environmental Investing’s issue (Vol. 10, No. 1, 2020) on climate and green bonds. Fixed-income securities that integrate environmental, social, and governance (ESG) factors have become a crucial component of most sustainable investment and climate-related risk management strategies. Global green bond issuance has grown from USD 87.2 billion in 2016 to USD 257.7 billion in 2019. However, this issue is addressing some of the challenges of rapid market scaling. The first pertains to the labeling of green bonds. Albeit the term “green bond” becoming synonymous for the entire spectrum of ESG-aligned fixed income securities, there now exists a plethora of labels, names, and designations for green bonds, often resulting in confusion about what exactly constitutes a green bond. By providing the most comprehensive overview to date of all green bond variants, this issue explores the core attributes of green bonds, such as their potential returns from financial and nonfinancial angles, taxonomical and underlying conceptual considerations, and academic assessments of the market as a whole. In conclusion, this paper and the corresponding issue provide contemporary insights and an up-to-date snapshot of the evolving characteristics of climate and green bonds.

1. Introduction

So far, 2020 has proven to be a year of profound global turmoil, affecting all aspects of human life. From the socio-economic Covid-19 disruptions and protests against racial inequality to the continuously escalating climate crisis, humanity is at a veritable crossroads in terms of addressing and remedying past, present, and future risks to society and the planet. With the Paris Climate Agreement and the UN Sustainable Development Goals (SDGs), the global community has established ambitious yet critical targets to safeguard and improve the lives of present and future generations. In order to achieve these goals, numerous stakeholders, including law- and policy-makers, industry and civil society representatives, and academia, have been developing and conceptualizing appropriate tools and strategies.

Financial instruments, and the financial sector in general, have been identified as major levers in contributing to the fight against global warming and sustainable development. In recent years, terms such as sustainable investing, sustainable finance, and impact investing have entered the investor vocabulary, indicating that sustainability, climate, and socio-environmental issues are gaining in relevance among industry practitioners. Environmental, social, and governance (ESG) factors, climate-related risks, and nonfinancial performance metrics have transformed from marginal into material investment considerations. Investors are now turning their attention to the different approaches and vehicles at their disposal to integrate ESG factors or manage environmental and climate-related risks in their portfolios.

Fixed-income securities that use their proceeds toward the financing of ESG-aligned projects have proven particularly attractive among investors. Their volume has been increasing exponentially since their inception by the European Investment Bank (EIB) in 2007 and following their expansion by the International Finance Corporation (IFC) in 2010. A 2019 study examines the publicly reported allocations of green bond proceeds from 53 organizations to projects and assets throughout 96 countries from 2008 to 2017 (Tolliver et al. 2019). It found that the projects and assets financed with green bonds in this study sample are associated with over 108 million tonnes of carbon dioxide equivalent (tCO2e) in greenhouse gas emission reductions and over 1,500 gigawatts in renewable energy capacity (Tolliver et al. 2019). Nowadays, the fixed-income securities category is represented throughout the entire investment chain, ranging from corporate bonds to municipal bonds and sovereign bonds. They seemingly offer a variety of advantages that render their issuance—as well as the measurement, reporting, and verification (MRV) of capital allocation and impact assessments—comparatively easier to accomplish than, for example, that of ESG-aligned funds or benchmark indexes.

For this special issue, we looked for articles that explore the extent to which sustainability-linked and ESG-aligned fixed-income securities can support the mainstreaming of responsible investment principles across the financial sector. We welcomed articles from practitioners, professionals, business leaders, regulators, and academics highlighting the transformative power of ESG-related bonds and the extent to which their often-unique characteristics have an impact on environmental investing as a whole.

Topics of particular interest and contemporary relevance have been: taxonomies; benchmarks; disclosure and reporting standards; impact measurement metrics; the roles of multilateral-development banks (MDBs) and development finance institutions (DFIs); public, private, and blended financing structures; the role of regulators; the role of stock exchanges; bond certification, ratings, and labels; classes of ESG-related bonds; and eligibility criteria. The final submissions analyze underexplored aspects and characteristics of ESG-aligned fixed-income securities and expand the dynamic conceptualizations of the latter. These will contribute to the growing body of academic literature on green and sustainability bonds.

Among the topics covered in their articles, the authors further investigate fundamental conditions that need to be fulfilled for fixed-income securities to be considered ESG-aligned, generate a tangible sustainability-related impact, and remain attuned with conventional market-level financial performance metrics. These are challenges facing many issuers of green bonds[1] and other sustainability-linked bond variants. By taking into account ESG factors, such as climate-related risks, green bonds have the potential to outperform their conventional peers because they are less exposed or vulnerable to negative ESG externalities.

In order to contextualize the articles of this special issue, it is important to outline the current understanding and developments around green bonds.

[1] The term “green bond” will be utilized representatively for all ESG-aligned fixed-income securities throughout this article.

2. What Exactly Renders a Bond Green?

As mentioned above, the core concept of what is known today as a green bond emerged in 2007, when the EIB issued “Climate Awareness Bonds” (CABs). It bore the peculiar characteristic that its proceeds were earmarked and ring-fenced toward contributing to climate action in renewable energy and the energy efficiency sector (EIB 2020). The World Bank Group then incorporated a similar principle in their own sustainability-linked fixed-income product, the original “Green Bond.” It was the first financial product that used the designation “green bond,” and its first round was issued in 2010. All subsequent variants of green bonds then followed the core financial principles set out by the EIB’s CABs and the IFC’s Green Bonds. In theory, green bonds have higher yields and lower variance, and are more liquid, if compared with their closest brown bond neighbors (Bachelet et al. 2019). But a negative premium was dependent on the green bonds’ being issued either by large institutional issuers or by private issuers whose bonds had external third-party verification (Bachelet et al. 2019). However, some issuers have been advocating for a “greenium” that investors should pay and that would cover the additional cost associated with pre-issuance (ex-ante) third-party and post-issuance(ex-post) impact monitoring and reporting (Weber and Saravade 2019). Still, Gianfrate and Peri (2019) observed that green bonds are actually more convenient than conventional bonds because the magnitude of the savings for issuers (in terms of interests paid) exceeds the costs of getting third-party certification or verification.

The global green bond market has seen rapid growth, with total issuance increasing from USD 87.2 billion in 2016 to USD 257.7 billion in 2019 (CBI 2017; 2019d). The United States, China, and France accounted for the majority of issuances according to the Climate Bonds Initiative (CBI) tracking figures (CBI 2017; 2019d). Supranational entities, notably MDBs and DFIs, also accounted for a significant share of issuance volume, standing at USD 13.7 billion in 2019, which represents 7% growth compared to 2018 (CBI 2019d). This solidified their precursory role in the market by facilitating new types of ESG-related bond types. A lot of this growth has also been catalyzed by stock exchanges with the first EIB CAB being listed at the Luxembourg Stock Exchange (LuxSE) in 2007 (Erhart 2018a). Many exchanges have been observed listing green bonds without any additional listing fees, as compared to vanilla bonds, and despite additional listing requirements in terms of verification and document screening (Erhart 2018a; 2018b).

Nonetheless, the overall size of the green bond market still pales in comparison to the conventional bond market, for which new bond issuance in 2019 totaled USD 6.86 trillion, up 17% from 2018 (S&P Global 2020). This solidified their precursory role in the market by facilitating new types of ESG-related bond types. However, these figures and greenwashing challenges, such as the inclusion of projects related to “clean coal” that were permitted for many Chinese green bonds, lead us to some of the key issues around standardization inconsistencies addressed in this JEI special issue (Weber and Saravade 2019).

Because rules and frameworks pertaining to domestic green securities inside China have at times differed substantially from international standards, significant dilemmas have arisen for investors interested in ESG-aligned portfolios (Weinland 2020). The main difference concerned coal-fired power generation, since Chinese green bond guidelines did not exclude investments in “ultra-super-critical” coal-fired power (CBI 2020a; 2020c). This approach starkly contrasts with the two predominant international standards, the CBI Standards and the ICMA (International Capital Markets Association) Green Bond Principles, both of which exclude coal-fired power generation projects on the basis of their misalignment with emissions scenarios set by the Paris Climate Agreement and multiple other negative externalities linked to their operation, such as air pollution and mineral extraction (CBI 2020b; ICMA 2018b). This situation sometimes required trading platforms to make adjustments in order to account for these taxonomical divergences. For example, the LuxSE, which created the first dedicated Green Bond Exchange (LGX) in 2016, cross-listed Chinese green securities separately from regular ones on its platform. (LuxSE 2020). LuxSE indicated (among others) that the Green Bond Endorsed Project Catalogue by the People’s Bank of China (PBOC), one of China’s main financial regulators, “accepts retrofits of fossil fuel power stations, clean coal and coal efficiency improvements, and rail lines that mainly transport fossil fuels, which are not accepted under the Climate Bonds Initiative’s eligibility taxonomy” (LuxSE 2020). Some studies found that these differences may affect the lender’s investment assessment and decision on whether to provide financing to the issuer (Zhang 2020).

In a major apparent and imminent policy reversal, a draft for consultation of the 2020 edition of the PBOC’s Green Bond Endorsed Projects Catalogue dropped fossil-fuel-related projects, including coal, from its taxonomy of eligible green projects (CBI 2020c). This development in China notwithstanding, the controversies around the inclusion of coal and other fossil-fuel-related projects are still continuing and touch directly on discussions surrounding greenwashing. Greenwashing in the ESG investing and sustainable finance industries alludes to the practice of marketing or distributing finance products or services that overstate their positive sustainability impacts, or understate their material environmental risks, or generally misrepresent their perceived ESG-related benefits. Reputational and economic considerations are the most frequent reasons for engaging in greenwashing. Several green bond products have been denounced as greenwashing attempts, notably a sustainability-linked bond by Italian energy conglomerate Enel (EF 2019a). In that instance, the greenwashing accusations made by large institutional investor Nuveen were not shared unequivocally; some researchers claimed that while certainly improvable, Enel’s bond in question presented more comprehensive target-setting and incentives to reach the latter than conventional green bonds offered up to that moment (Dupré 2019). The controversies and discussions surrounding the inflation in green bond labels and designations were covered comprehensively by several commentators who observed that all of the innovation and experimentation in this area can lead to a simultaneous growth of greenwashing risks if no proper standards are fixed for the green bond market (Cripps 2019; Lee 2020; Deschryver and De Mariz 2020). Bonds issued by companies operating in carbon-intensive sectors, such as Enel, Repsol, Snam, and Teekay with their fossil-fuel-related activities, or Marfrig, a Brazilian meat producer, were seen as particularly critical. Most critics questioned the sincerity of their transition efforts and the general use of proceeds toward carbon reductions and other SDG-related improvements (Cripps 2019; Robinson-Tillett 2019; Lee 2020).

3. United We Stand, Divided We Fall: Initiatives to Reduce Greenwashing

In light of these persisting systemic risks—emanating from greenwashing and the general fluidity in defining what makes a project eligible to be considered green or ESG-aligned—multiple financial market regulators then attempted to provide clear guidelines on what types of activities could benefit from green bond proceeds. Prominent examples include the Japanese Ministry of Environment, which issued the first iteration of the Green Bond Guidelines in 2017, and the European Union (EU), which started a process at the end of 2016, with the creation of the High-Level Expert Group on Sustainable Finance (HLEG), to develop an overarching and comprehensive EU strategy on sustainable finance, including for green bonds (MOEJ 2017; EC 2018). The EU’s efforts then culminated in concrete recommendations for the introduction of an EU Green Bond Standard (GBS), published in 2019 after prior preparatory work by a Technical Expert Group (TEG), a follow-up to the HLEG (EC 2020a; 2020d). The EU’s GBS referenced the EU Taxonomy, a “classification system for sustainable economic activities—that will create a common language that investors can use everywhere when investing in projects and economic activities that have a substantial positive impact on the climate and the environment” (EC 2020b; 2020c).

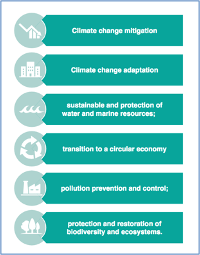

For projects to be eligible under the EU GBS, issuers need to demonstrate how the raised capital will actually be employed. While “use-of-proceeds” is not new, for the CBI and the ICMA pursued a similar approach in their respective guidelines and standards, the EU went a step further by tying any green-bond-related “use-of-proceeds” to projects and activities aligned with the Taxonomy (EC 2020c). This means that projects, in order to be eligible for inclusion in green bond financing, need to comply with several conditions (Figure 1) and environmental objectives (Figure 2).

Figure 1. EU Sustainable Finance Taxonomy—Performance Thresholds (referred to as ‘technical screening criteria’)

Figure 2. EU Sustainable Finance Taxonomy—Six Environmental Objectives

In climate change mitigation, the taxonomy also sets several sectoral criteria; it sets, for example (EC 2020b):

- The emissions intensity threshold of 100g CO2e / kWh is proposed for electricity generation, heat production and the co-generation of heat and electricity. This threshold will be reduced every five years in line with political targets set out to achieve net-zero emissions by 2050.

- For passenger cars and light commercial vehicles:

- Zero tailpipe emission vehicles (including hydrogen, fuel cell, electric). These are automatically eligible.

- Vehicles with tailpipe emission intensity of max 50 g CO2/km (WLTP) are eligible until 2025.

- From 2026 onwards only vehicles with emission intensity of 0g CO2/km (WLTP) are eligible.

The EU GBS and the corresponding EU Taxonomy represent thus far the most elaborate attempt at creating a uniform, and mandatory, set of rules and standards for green bonds. They are meant to provide investors with certainty around the ESG-alignment of the projects that respective green bond fund managers will invest in.

While standards regarding green fixed-income securities can increase the level of transparency in the ESG-investing and sustainable finance sectors, the fracturing of green bonds into continuously growing numbers of sub-groups and label variants hinders rather than supports broader awareness around green bonds.

Particular issues are the multiple label, denominations, and designations that have appeared for green bonds ever since their conceptual inception and practical implementation in 2007 by the EIB. The EIB marketed their first issuance of green bonds as “Climate Awareness Bonds” (CABs) in 2007, focusing mainly on climate-related projects (EIB 2020b). These were then complemented by “Sustainability Awareness Bonds” (SABs) in 2018, which responded to the EU’s Action Plan on Sustainable Finance and have a stronger focus on the SDGs at large by aligning with the ICMA’s Social Bond Principles and Sustainability Bond Guidelines (EIB 2018; 2019; 2020c). In 2018 and 2019, SAB project allocations were almost exclusively water-related; the majority of projects dealt with water supply, sewage, and wastewater collection and/or treatment (EIB 2018; 2019; 2020c).

However, the EIB-issued CABs and SABs constitute only two forms of currently marketed ESG-aligned fixed-income securities. Over the years, we have seen a plethora of green bond variants being launched. They all share commonalities in terms of “use-of-proceeds” frameworks and, in some form or shape, have to contribute to sustainability goals or integrate ESG factors to varying degrees (Table 1). These green bond variants often also follow or align with different guidelines or frameworks, which renders a general understanding of the underlying principles of green bonds unnecessarily complex (Table 1). This complexity risks exacerbating the challenges that green bonds still face in the market: first, protecting their environmental integrity, and second, enhancing their financial benefits (I4CE 2016). The increasing variety of bonds also corresponds to the regional risks that issuers anticipate in emerging markets and developing countries (Weber and Saravade 2019). While many sustainability and SDG-related projects would be carried out in these regions, some issuers remain cautious as to whether they can uphold investor expectations regarding transparency and disclosures to avoid any issues related to accountability. Hence, they see the diversification of bond types as a way of risk management (Weber and Saravade 2019).

Table 1. List of Green Bond Variants / Labels (in alphabetical order

As the extensive, albeit non-exhaustive, list in Table 1 shows, the green bond ecosystem is gradually becoming more multifaceted and the labels utilized by issuers are rapidly expanding to cover a growing number of SDG-related indicators or ESG factors at a more granular level. For example, green convertible bonds are the latest innovation in this bond segment. They have already gained prominence in areas of project finance for green energy infrastructure and green buildings (Fioretti 2019; Gregor, 2020).

In this context, new regulatory proposals such as the EU Taxonomy and EU GBS, as well as efforts by the International Standards Organization (ISO) Technical Committees 207 (Environmental Management) and 322 (Sustainable Finance), aim at creating uniform frameworks and standards that will reduce greenwashing and will increase transparency and the comparability of ex-ante project-related impact assessments and ex-post impact-related data collection. (ISO 2018; 2020). Post-issuance reporting is particularly important in measuring the veritable impacts of projects financed by green bond funds. Tolliver et al. (2019) concluded that many institutions still fail to publish reports that articulate environmental impact estimates of proceeds-recipient projects and assets. They stated that many post-issuance reports do not clearly identify the additionality of green bond impacts, which renders it difficult to derive the connections between SDGs and Nationally Determined Contributions (NDCs) oriented to environmental outcomes and green bond finance vehicles (Tolliver at al. 2019). These sentiments are echoed by Sartzetakis (2020), who states that bridging the informational gap between issuers and investors is probably the most important challenge for green bonds at the moment. Providing clear green criteria and a comprehensive monitoring process (for example, information on the projects’ environmental impact) is crucial to the scaling of the green bond market.

Therefore, a lot of work remains: although a 2019 report found significant improvements over the past years by issuers providing use-of-proceeds or post-issuance impact reports, the scope and granularity of these reports need to be fundamentally improved (CBI 2019c). In order to draw proper conclusions about the material nonfinancial impacts of green bond-funded projects, the collected data requires further standardization and detail. Apart from the EU and the ISO, the industry-led ICMA has also proposed new harmonized frameworks on green and social bonds to enhance the usability of existing guidance on impact reporting and to avoid repetitions (ICMA 2020a; 2020b).While all of these initiatives are generally seen as steps in the right direction to counter greenwashing and stimulate sustainable investing, countries that still have non-negligible stakes in carbon-intensive industries are cautious because the Taxonomy’s rigid sectoral thresholds would, for example, lead to the complete exclusion of coal, oil, and most gas projects and operations (CBI 2019b; EC 2020b; EC 2020c).

Japan, among others, has been particularly vocal since the country still relies heavily on coal for its domestic energy production, besides being a major exporter of coal-fired power-plant technology to other Asian countries (Schumacher et al. 2020; InfluenceMap 2020). In light of these facts, and despite having announced it will shut down about 100 inefficient coal plants by 2030, the Japanese Ministry of Energy, Trade and Industry (METI), in collaboration with several energy policy researchers, went on to propose a Climate Transition Finance Principle (Nikkei Asian Review 2020; Responsible Investor 2020). These principles act as a counterbalancing agent to the EU Taxonomy in that they explicitly permit the use of proceeds for transition actions toward the de- or low-carbonization of GHG-emitting industries and sectors (METI 2020). These views have also been supported by a number of studies; for example, Demary and Neligan (2019) argued in favor a more flexible and gradual approach when defining which economic activities are green and which are non-green. They advocate that businesses should, at least in part, be allowed to issue green bonds if they invest in technologies that reduce their CO2-emissions significantly (Demary and Neligan 2019).

In addition to Japan, other countries have also proposed their own sustainable finance principles to define which activities fall under the sustainable finance moniker (CBI 2019b). Canada, like Japan, has also proposed the establishment of a “Transition Finance Taxonomy,” complementing a regular EU-style green finance taxonomy (Canada Government 2019; CSA Group 2020). In south-east Asia, Malaysia has proposed a “Climate Change and Principle-based Taxonomy” that directly incorporates elements from the EU taxonomy, including the “do-no-significant-harm” principle (BNM 2019).

4. The Climate/Green Bonds Special Issue: Outline and Discussion

These examples illustrate the need for further structuring and clarifications concerning green bonds. Otherwise, numerous stakeholders and the general public will find it challenging to fully decipher the increasingly complex language and principles found across the green-bond spectrum. Academia, situated at the intersection of applied business-oriented research and the exploration of theoretical concepts in sustainable and environmental investing, plays an important role, both as a mediator between the scientific and business communities, and as an essential provider of ESG data.

This JEI special issue contains detailed case studies, literature reviews, and discussions that provide in-depth examinations of the green and climate bonds market and how certain aspects have evolved. They range from liquidity-level investigations around a specific type of forest sustainability bond in the first paper to the second paper’s concept of greenium and whether market pricing mechanisms deliver an advantage to the cost of capital for green bonds. The next paper then provides an extensive review on the development of independent market-level sustainable finance taxonomy, while the final paper is a conceptual analysis of the core structures that underlie the green bond market.

To provide additional context and discussion, an expert opinion accompanies each article. These comment pieces, written by current industry practitioners, financial sector stakeholders, and academic experts, complement each article not only by discussing or challenging its methodologies and results but also by outlining potential avenues for further research and stakeholder engagement.

Biography

Dr. Kim Schumacher is a Lecturer in Sustainable Finance and ESG at the Tokyo Institute of Technology. His research focuses on ESG data and impact metrics, sustainable finance frameworks, green bonds, natural capital valuation, ecosystem services, renewable energy project development, and TCFD disclosure. In addition, he is an Honorary Research Associate at the School of Geography and the Environment, University of Oxford.

From May 2019 to May 2020, he was also a consultant for the Luxembourg Ministry of the Environment, Climate and Sustainable Development. Prior, he conducted post-doctoral research as part of the Economics of Sustainability and Sustainable Finance programmes at the Smith School of Enterprise and the Environment, University of Oxford.

He is a Chartered Environmentalist (CEnv) and sits on the ISO Technical Committees on Sustainable Finance (TC 322) and Environmental Management (TC 207). He belongs to the Technical Working Groups of the Climate Disclosure Standards Board (CDSB), the Climate Bonds Initiative (CBI), and the Green Finance Network Japan (GFNJ). He holds a PhD degree in Environmental Science from the University of Tokyo (2017) and a Master’s degree in Environmental Law and Policy from UC Berkeley (2012).

References

Al Mheiri, W., and H. Nobanee. 2020. “Green Bonds: A Mini-Review.” Available from SSRN Electronic Journal at https://doi.org/10.2139/ssrn.3538790.

Bachelet, M. J., L. Becchetti, and S. Manfredonia. 2019. “The Green Bonds Premium Puzzle: The Role of Issuer Characteristics and Third-Party Verification.” Sustainability 11(4) 1–22. Available from https://doi.org/10.3390/su11041098.

BBVA. 2018. “Sustainable Development Goals (SDGs): Bond Framework.” Available from https://accionistaseinversores.bbva.com/wp-content/uploads/2018/04/BBVA-SDGs-Bond-Framework_23042018_Eng.pdf.

BBVA. 2019. “ESG Bonds: Key Topics and Trends for 2019 and Beyond.” Available from https://www.bbva.com/en/esg-bonds-key-topics-and-trends-for-2019-and-beyond/.

BBVA. 2020. “BBVA Raises €1bn in First-ever Green CoCo Bond by a Financial Institution.” Available from https://www.bbva.com/en/bbva-is-the-first-financial-institution-in-the-world-to-issue-green-coco-bonds/.

BNM (Bank Negara Malaysia/Central Bank of Malaysia). 2019. “Climate Change and Principle-Based Taxonomy.” Discussion Paper. Available from https://www.bnm.gov.my/index.php?ch=57&pg=144&ac=894&bb=file.

BNP Paribas. 2019. “Italian Energy Company Issues Groundbreaking SDG-linked Bond.” Available from https://cib.bnpparibas.com/sustain/italian-energy-company-issues-groundbreaking-sdg-linked-bond_a-3-3063.html.

Canada Government. 2019. Final Report of the Expert Panel on Sustainable Finance: Mobilizing Finance for Sustainable Growth. Monograph. Available from http://publications.gc.ca/collections/collection_2019/eccc/En4-350-2-2019-eng.pdf.

CBI (Climate Bonds Initiative). 2017. “Green Bond Highlights 2017.” London: Climate Bonds Initiative, January 2018. Available from https://www.climatebonds.net/files/reports/cbi-green-bonds-highlights-2017.pdf.

CBI. 2018. “CBI Green Bond Database Methodology.” London: Climate Bonds Initiative, September 2018. Available from https://www.climatebonds.net/files/files/Climate-Bonds-Initiative_GreenBondMethodology_092018%281%29.pdf.

CBI. 2019a. Climate Bonds Standard Version 3.0: International Best Practice for Labeling Green Investments. London: Climate Bonds Initiative. Available from https://www.climatebonds.net/files/files/climate-bonds-standard-v3-20191210.pdf.

CBI. 2019b. “Growing Green Bond Markets: The Development of Taxonomies to Identify Green Assets.” London: Climate Bonds Initiative. Available from http://greenbondplatform.env.go.jp/pdf/CBI%20_Taxonomy_final.pdf.

CBI. 2019c. Post-Issuance Reporting in the Green Bond Market. London: Climate Bonds Initiative. Available from https://www.climatebonds.net/files/reports/cbi_post-issuance-reporting_rev092019_en_0.pdf.

CBI. 2019d. “2019 Green Bond Market Summary.” London: Climate Bonds Initiative. Available from https://www.climatebonds.net/files/reports/2019_annual_highlights-final.pdf.

CBI. 2019e. Climate Resilience Principles: A Framework for Assessing Climate Resilience Investments. London: Climate Bonds Initiative. Available from https://www.climatebonds.net/files/page/files/climate-resilience-principles-climate-bonds-initiative-20190917-.pdf.

CBI. 2020a. “China’s Top Regulators Announce They Will Exclude Fossil Fuels from Their Green Bonds Taxonomy. It’s a Major Development!” London: Climate Bonds Initiative. Available from https://www.climatebonds.net/2020/06/chinas-top-regulators-announce-they-will-exclude-fossil-fuels-their-green-bonds-taxonomy-it.

CBI. 2020b. “Climate Bonds Standard—Frequently Asked Questions.” London: Climate Bonds Initiative. Available from https://www.climatebonds.net/standard/faqs.

CBI. 2020c. Green Bond Endorsed Projects Catalogue (2020 edition). Draft for consultation. Climate Bonds Initiative. Available from https://www.climatebonds.net/files/files/China-Green-Bond-Catalogue-2020-Consultation.pdf.

CEB (Council of Europe Development Bank). 2018. “CEB Publishes Report on First Social Inclusion Bond.” Paris: Council of Europe Development Bank. Available from https://coebank.org/en/news-and-publications/news/ceb-publishes-report-first-social-inclusion-bond/.

CEB. 2020. Council of Europe Development Bank Social Inclusion Bond Framework. Paris: Council of Europe Development Bank. Available from https://coebank.org/documents/942/CEB_Social_Inclusion_Bond_Framework_update_Apr2020.pdf.

Council of the European Union. 2020. “Position of the Council at first reading with a view to the adoption of a Regulation of the European Parliament and of the Council on the establishment of a framework to facilitate sustainable investment, and amending Regulation (EU) No. 2019/2088.” Available from https://data.consilium.europa.eu/doc/document/ST-5639-2020-INIT/en/pdf.

Cripps, P. 2019. “Green Bond Comment, November 2019: A Market in Transition.” Environmental Finance (06 November, 2019). Available from https://www.environmental-finance.com/content/analysis/green-bond-comment-november-2019-is-this-the-beginning-of-the-end-of-the-green-bond-market.html.

CSA Group. 2020. “Defining Transition Finance in Canada.” Available from https://www.csagroup.org/news/defining-transition-finance-in-canada/.

Demary, M., and A. Neligan. 2019. Defining Green Bonds: The Danger of Neglecting the Issuer Side—Looking at Problems and Solutions. IW-Policy Paper, No. 2/2019. Köln: Institut der deutschen Wirtschaft (IW) / German Economic Institute. Available from https://www.iwkoeln.de/fileadmin/user_upload/Studien/policy_papers/PDF/2019/IW-Policy-Paper_2019_Defining_Green_Bonds.pdf.

Deschryver, P., and F. de Mariz. 2020. “What Future for the Green Bond Market? How Can Policymakers, Companies, and Investors Unlock the Potential of the Green Bond Market?” in Green and Sustainable Finance, issue of Journal of Risk and Financial Management,13(3), 61. Available from https://doi.org/10.3390/jrfm13030061.

Dupré, S. 2019. “In Response to Accusations that Enel’s SDG Bond Was Greenwashing.” Environmental Finance (31 October, 2019). Available from https://www.environmental-finance.com/content/analysis/in-response-to-accusations-that-enels-sdg-bond-was-greenwashing.html.

EBRD (European Bank for Reconstruction and Development). 2019a. “World’s First Dedicated Climate Resilience Bond, for US$ 700m, Is Issued by EBRD,” by Varnora Bennett. Available from https://www.ebrd.com/news/2019/worlds-first-dedicated-climate-resilience-bond-for-us-700m-is-issued-by-ebrd-.html.

EBRD. 2019b. Investor Information: Green and Social Bonds. Sustainability Report 2019. European Bank for Reconstruction and Development. Available fromhttps://2019.sr-ebrd.com/investor-information-green-and-social-bonds.

EBRD. 2020. Focus on Environment. European Bank for Reconstruction and Development. Available from https://www.ebrd.com/focus-on-environment.pdf.

EC (European Commission). 2018. Action Plan: Financing Sustainable Growth. Commission action plan on financing sustainable growth: Final text. Luxembourg: European Commission. Available from https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52018DC0097&from=EN.

EC. 2020a. “Sustainable Finance: Commission Welcomes the Adoption by the European Parliament of the Taxonomy Regulation.” Luxembourg: European Commission. Available from https://ec.europa.eu/commission/presscorner/detail/en/ip_20_1112.

EC. 2020b. Taxonomy Report: Technical Annex. Luxembourg: European Commission. Available from https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/200309-sustainable-finance-teg-final-report-taxonomy-annexes_en.pdf.

EC. 2020c. Taxonomy: Final Report of the Technical Expert Group on Sustainable Finance. Luxembourg: European Commission. Available from https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/200309-sustainable-finance-teg-final-report-taxonomy_en.pdf.

EC. 2020d. Usability Guide: EU Green Bond Standard. Luxembourg: European Commission. Available from https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/200309-sustainable-finance-teg-green-bond-standard-usability-guide_en.pdf.

EIB (European Investment Bank). 2016. Climate Awareness Bonds Statement for the Year Ended December 31, 2015. Luxembourg: European Investment Bank. Available from https://www.eib.org/attachments/fi/cab-statement-2015.pdf.

EIB. 2017. “European Investment Bank Climate Action: List of Eligible Sectors and Eligibility Criteria.” Luxembourg: European Investment Bank. Available from https://www.eib.org/attachments/strategies/climate_action_lending_eligibility_list_en.pdf.

EIB. 2018. EIB Issues First Sustainability Awareness Bond, Luxembourg: European Investment Bank. Available from https://www.eib.org/en/press/all/2018-223-eib-issues-first-sustainability-awareness-bond.

EIB. 2019. EIB Sustainability Awareness Bonds: Capital Market Presentation. Luxembourg: European Investment Bank. Available from https://www.eib.org/attachments/fi/0_sab_website.pdf.

EIB. 2020a. “CAB with EU Taxonomy-Compliant Documentation Reaches Benchmark Status in EUR.” Luxembourg: European Investment Bank. Available from https://www.eib.org/en/investor_relations/press/2020/fi-2020-18-eib-tap-eur-cab-2042.htm.

EIB. 2020b. “Climate Awareness Bonds.” Luxembourg: European Investment Bank. Available from https://www.eib.org/en/investor_relations/cab/index.htm.

EIB. 2020c. “Sustainability Awareness Bonds.” Available from https://www.eib.org/en/investor_relations/sab/index.htm.

Environmental Finance. 2019a. “Enel’s Sustainability Bond Was Greenwashing, Says Nuveen.” Available from https://www.environmental-finance.com/content/news/enels-sustainability-bond-was-greenwashing-says-nuveen.html.

Environmental Finance. 2019b. Sustainable Bonds Insight 2019. Available from https://www.environmental-finance.com/assets/files/SUS%20BONDS%20INSIGHT%20FINAL-final.pdf.

Environmental Finance. 2020. Sustainable Bonds Insight 2020. Available from https://www.environmental-finance.com/assets/files/research/sustainable-bonds-insight-2020.pdf.

Erhart, S. 2018a. “Exchange-Traded Green Bonds.” Discussion paper. The Journal of Environmental Investing. Available from https://www.thejei.com/wp-content/uploads/2018/10/Exchange-Traded-Green-Bonds-by-Szilard-Erhart.pdf.

Erhart, S. 2018b. Exchange Traded Green Bonds, Mendeley Data, v1. Available from http://dx.doi.org/10.17632/y49w92dzh3.1.

Fidelity International. 2019. “Sustainable Investors Should Wake Up to Companies in Transition,” by Kristian Atkinson. Available from https://www.fidelityinternational.com/editorial/blog/sustainable-investors-should-wake-up-to-companies-in-transition-a3c4f0-en5/.

Fioretti, J. 2019. “Link REIT Raises $510 mln in Largest Green Convertible Bond Globally.” Reuters, March 8, 2019. https://www.reuters.com/article/link-reit-convertible-bonds/link-reit-raises-510-mln-in-largest-green-convertible-bond-globally-idUSL5N20V0CK.

Gianfrate, G., and M. Peri. 2019. “The Green Advantage: Exploring the Convenience of Issuing Green Bonds.” Journal of Cleaner Production 219 (May): 127–135. Available from https://doi.org/10.1016/j.jclepro.2019.02.022.

Gregory, A. 2020. “Nascent Green Convertible Bond Market Is Cause for Optimism.” Global Capital (July 23). Available from https://www.globalcapital.com/article/b1mlj4w7k0rfg9/nascent-green-convertible-bond-market-is-cause-for-optimism.

Gross, A., and T. Stubbington. 2020. “The ‘Transition’ Bonds Bridging the Gap between Green and Brown.” Available from https://www.ft.com/content/ff2b3e88-21b0-11ea-92da-f0c92e957a96.

I4CE (Institute for Climate Economics). 2016. Beyond Transparency: Unlocking the Full Potential of Green Bonds, by I. Shishlov, R. Morel, and I. Cochran. Institute for Climate Economics. Available from https://www.i4ce.org/wp-core/wp-content/uploads/2016/06/I4CE_Green_Bonds-1.pdf.

ICMA (International Capital Market Association). 2018a. Sustainability Bond Guidelines. Paris: International Capital Market Association. Available from https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/Sustainability-Bonds-Guidelines-June-2018-270520.pdf.

ICMA. 2018b. Green Bond Principles: Voluntary Process Guidelines for Issuing Green Bonds. Paris: International Capital Market Association. Available from https://www.ifc.org/wps/wcm/connect/cef061f1-6406-4a11-8dd3-2d4a6c47e66c/Green+Bond+Principles+-+June+2018+140618+WEB.pdf?MOD=AJPERES&CVID=n4SKWF8.

ICMA. 2019. “2019/2020 Working Group Climate Transition Finance.” Paris: International Capital Market Association. Available from https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/Climate-Transition-Finance-WG-ToR-FINAL221119.pdf.

ICMA. 2020a. Handbook: Harmonized Framework for Impact Reporting. Paris: International Capital Market Association and the Green Bonds Principles. Available from https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/Handbook-Harmonized-Framework-for-Impact-Reporting-220520.pdf.

ICMA. 2020b. Working Towards a Harmonized Framework for Impact Reporting for Social Bonds. Paris: International Capital Market Association. Available from https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/June-2020/Harmonized-Framework-for-Impact-Reporting-for-Social-BondsJune-2020-090620.pdf.

ICMA. 2020c. Social Bond Principles: Voluntary Process Guidelines for Issuing Social Bonds. Paris: International Capital Market Association. Available from https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/June-2020/Social-Bond-PrinciplesJune-2020-090620.pdf.

ICMA. 2020d. Sustainability-Linked Bond Principles: Voluntary Process Guidelines. Paris: International Capital Market Association. Available from https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/June-2020/Sustainability-Linked-Bond-PrinciplesJune-2020-100620.pdf.

IDA (International Development Association). 2020. “IDA Debuts in Sterling with Successful GBP 1.5 Billion 5-year Benchmark Bond.” Washington, DC: The World Bank (January 16, 2020). Available from https://www.worldbank.org/en/news/press-release/2020/01/16/ida-debuts-in-sterling-with-successful-gbp-1-5-billion-5-year-benchmark-bond.

IFC (International Finance Corporation). 2019. IFC Forests Bond Annual Report to Bond Investors. Summary Based on Annual Monitoring Report Prepared by Wildlife Works Carbon LLC. Washington, DC: International Finance Corporation. Available from https://www.ifc.org/wps/wcm/connect/df70d1fd-c831-480a-9ef4-76306c933111/IFC+Forests+Bond++Annual+Report_July+2018-+June+2019_Final.pdf?MOD=AJPERES&CVID=n0LHTmg.

IFC. 2020a. “Social Bonds.” Washington, DC: International Finance Corporation. Available from https://www.ifc.org/wps/wcm/connect/corp_ext_content/ifc_external_corporate_site/about+ifc_new/investor+relations/ir-products/socialbonds.

IFC. 2020b. “IFC Social Bond Framework.” Washington, DC: International Finance Corporation. Available from https://www.ifc.org/wps/wcm/connect/corp_ext_content/ifc_external_corporate_site/about+ifc_new/investor+relations/ir-products/ifc+social+bond+framework.

IFC. 2020c. “Forest Bonds.” Washington, DC: International Finance Corporation. Available from https://www.ifc.org/wps/wcm/connect/corp_ext_content/ifc_external_corporate_site/about+ifc_new/investor+relations/ir-products/forest_bonds.

IFC. 2020d. Green Bond Impact Report: Financial Year 2019. Washington, DC: International Finance Corporation. Available from https://www.ifc.org/wps/wcm/connect/90e2d0c8-8290-46a9-9e89-85335051c12a/Final+FY19+GBIR+-+6+Sep+2019.pdf?MOD=AJPERES&CVID=mQ7oWOr.

InfluenceMap. 2020. “How Japanese Industry Lobbied Against a Strong EU Taxonomy.” London: InfluenceMap. Available from https://content.influencemap.org/report/-2a321cd8bdc7bd87c6a41a86fbfe62e9.

ISO (International Standards Organization). 2018. “The Secret to Unlocking Green Finance,” by Rick Gould. ISOfocus, 8 May, 2018. Available from https://www.iso.org/news/ref2287.html.

ISO. 2020. “Building a Framework for a Sustainable Future.” ISOfocus, 9 January, 2020. Available from https://www.iso.org/news/ref2469.html.

“Knowledge Is Power.” See UBS Optimus Foundation.

Lee, J. 2020. “Green Bonds Need the Right Filter.” Wall Street Journal, July 1, 2020.Available from https://www.wsj.com/articles/green-bonds-need-the-right-filter-11593509402.

LuxSE (Luxembourg Stock Exchange). 2020. “Chinese Domestic Green Securities.” LuxSE Group. Available from https://www.bourse.lu/chinese-domestic-green-securities.

Mair, V. 2017. “Investors in Peterborough Prison Bond, the World’s First Social Impact Bond, to Get 3% Return.” Responsible Investor, July 27, 2017. Available from https://www.responsible-investor.com/articles/peterboro-sib.

McVeigh, K. 2020. World Bank’s $500m Pandemic Scheme Accused of ‘Waiting for People to Die’ The Guardian, 28 February, 2020. Available from https://www.theguardian.com/global-development/2020/feb/28/world-banks-500m-coronavirus-push-too-late-for-poor-countries-experts-say.

METI (Ministry of Economy, Trade, and Industry). 2020. “Concept Paper on Climate Transition Finance Principles.” Study Group on Environmental Innovation Finance in Japan, March 2020. Available from https://www.meti.go.jp/press/2019/03/20200331002/20200331002-2.pdf.

MOEJ (Ministry of the Environment, Japan). 2017. Green Bond Guidelines 2017. MOEJ, March 28, 2017. Available from https://www.env.go.jp/en/policy/economy/gb/guidelines.html.

MOEJ. 2020. Green Bond Guidelines 2020 and Green Loan and Sustainability Linked Loan Guidelines 2020. MOEJ. Available from http://www.env.go.jp/policy/guidelines_set_version_with%20cover.pdf.

Naumann, B. 2019. “Investors Balk at Green Bond from Group Specializing in Oil Tankers. Financial Times, October 2019. Available from https://www.ft.com/content/b1d4201c-f142-11e9-bfa4-b25f11f42901.

Neoen. 2020. “Neoen launches the first ever European Green Convertible Bond issue for a maximal nominal amount of €170 million.” Neoen media release (Paris), May 27, 2020. Available from https://www.neoen.com/var/fichiers/1590595745-launch-pr-green-cb-neoen.pdf.

NIB (Nordic Investment Bank). 2019a. NIB Environmental Bond Report. Available from https://www.nib.int/filebank/a/1580366559/28a4c0a04e8d45d2c72b2d7c0f9985ec/10021-NIB_Environmental_Bond_Report_2019.pdf.

NIB. 2019b. NIB Environmental Bond Framework. Available from https://www.nib.int/filebank/a/1543996700/079a1634ef3203c6275f3225f1125fe8/9096-NEB_Framework_Dec_2018.pdf.

Nikkei Asian Review. 2020. “Japan Seeks Stoppage of 100 Inefficient Coal Plants in a Decade.” Nikkei Asian Review, July 2, 2020. Available from https://asia.nikkei.com/Business/Energy/Japan-seeks-stoppage-of-100-inefficient-coal-plants-in-a-decade.

Pimco. 2019. “SDG Bonds: Their Time Has Come,” by S. Mary, C. Schuetz, and O. Albrecht. Pimco Viewpoints, October 28, 2019. Available from https://global.pimco.com/en-gbl/insights/viewpoints/sdg-bonds-their-time-has-come.

Pratsch, M. 2020. “The 2020s—The Decade of Sustainable Bonds.” Environmental Finance, 11 February 2020. Available fromhttps://www.environmental-finance.com/content/the-green-bond-hub/the-2020s-the-decade-of-sustainable-bonds.html.

Reuters. 2008. “Disaster Bonds Seen Credit Market Bright Spot,” by Simon Challis. Reuters (London), January 10, 2008. Available from https://www.reuters.com/article/businesspro-insurance-bonds-dc/disaster-bonds-seen-credit-market-bright-spot-idUSL1041936020080110.

Robinson-Tillett, S. 2019. Analysis: IPCC Warning on Meat Consumption Adds to Scrutiny of Beef Producer Marfrig’s $500m ‘Transition Bond.’ Responsible Investor, August 8, 2019. Available from https://www.responsible-investor.com/articles/marfrig.

S&P Global. 2020. Credit Trends: Global Financing Conditions: Bond Issuance Is Expected to Grow 3.8% in 2020, ratings research by Nick W Kraemer, Sudeep K Kesh, Zev R Gurwitz, and Kirsten R Mccabe; leveraged commentary and data by Taron Wade. S&P Global Ratings, 30 January, 2020. Available from https://www.spglobal.com/ratings/en/research/articles/200130-credit-trends-global-financing-conditions-bond-issuance-is-expected-to-grow-3-8-in-2020-11327333.

Sartzetakis, E. S. 2020. “Green Bonds as an Instrument to Finance Low Carbon Transition.” Economic Change and Restructuring, 2020. Available from https://doi.org/10.1007/s10644-020-09266-9.

Schumacher, K., H. Chenet, and U. Volz. 2020. “Sustainable Finance in Japan.” Journal of Sustainable Finance & Investment 10(2): 213-243. Available from https://doi.org/10.1080/20430795.2020.1735219.

Snam. 2019. “Snam: Successfully Launched the First Climate Action Bond in Europe.” Snam press release, 21 February 2019. Available from https://www.snam.it/en/Media/Press-releases/2019/climate-action-bond.html.

Snam. 2020. Transition Bond Framework. Snam S.p.A. (Italy), June 2020. Available from https://www.snam.it/export/sites/snam-rp/it/investor-relations/debito_credit_rating/file/Transition-bond-framework-2020.pdf.

Theron A. 2020. “AfDB Concludes $116m Nedbank SDG-Linked Bonds.” ESI Africa Journal, July 6, 2020. Available from https://www.esi-africa.com/industry-sectors/finance-and-policy/afdb-concludes-116m-nedbank-sdg-linked-bonds/.

Tolliver, C., A. R. Keeley, and S. Managi. 2019. “Green Bonds for the Paris Agreement and Sustainable Development Goals.” Environmental Research Letters 14(6). Available from https://doi.org/10.1088/1748-9326/ab1118.

UBS Optimus Foundation. 2019. “Knowledge Is Power: The World’s First Development Impact Bond in Education Surpasses Both Target Outcomes.” UBS Optimus Foundation. Available from https://www.ubs.com/global/en/ubs-society/philanthropy/optimus-foundation/driving-change/our-impact/development-impact-bond.html.

UN Global Compact. 2019a. “First SDG-Linked Bond Raises US$1.5 billion.” UN Global Compact Media (New York), September 6, 2019. Available from https://www.unglobalcompact.org/news/4471-09-06-2019.

UN Global Compact. 2019b. SDG Bonds: Leveraging Capital Markets for the SDGs. Prepared by the UN Global Compact Action Platform on Financial Innovation for the SDGs, 2019. Available from https://info.unglobalcompact.org/l/591891/sdgbondsreport/3bb7lk.

UNDP (United Nations Development Programme). 2020. Practice Assurance Standards for SDG Bonds. UNDP, 2020. Available from https://sdgimpact.undp.org/assets/20200430-Bonds-Standards-Final-Draft.pdf.

Weber, O., and V. Saravade. 2019. “Green Bonds: Current Development and Their Future.” Center for International Governance Innovation Paper no. 210 (January 2019): 1–32. Available from https://www.cigionline.org/sites/default/files/documents/Paper no.210_0.pdf.

Weinland, D. 2020. “Global Investors Prepare to Brave China’s Green Bond Minefield.” Financial Times, June 4, 2020. Available from https://www.ft.com/content/28c6b076-8eab-11ea-af59-5283fc4c0cb0.

World Bank. 2017a. “World Bank Launches First-Ever Pandemic Bonds to Support $500 Million Pandemic Emergency Financing Facility.” Washington, DC: The World Bank press release, June 28, 2017. Available from https://www.worldbank.org/en/news/press-release/2017/06/28/world-bank-launches-first-ever-pandemic-bonds-to-support-500-million-pandemic-emergency-financing-facility.

World Bank. 2017b. “World Bank Offers First Sustainable Growth Bonds for Retail Investors in Belgium.” Washington, DC: The World Bank press release, October 17, 2017. Available from https://www.worldbank.org/en/news/press-release/2017/10/19/world-bank-offers-first-sustainable-growth-bonds-for-retail-investors-in-belgium.

World Bank. 2018a. Demystifying Bonds for Debt Managers, prepared by Abigail Baca and Aki Jain. Washington, DC: The World Bank, IBRD, and IDA. Available from http://pubdocs.worldbank.org/en/555651528746619166/webinar-demystifyingcatastrophebondsfordebtmanagers2018-presentation-abigailbacaandakinchanjain.pdf.

World Bank. 2018b. “Seychelles Launches World’s First Sovereign Blue Bond.” The Republic of Seychelles/ Washington, DC/ Bali: October 29, 2018. Available from https://www.worldbank.org/en/news/press-release/2018/10/29/seychelles-launches-worlds-first-sovereign-blue-bond.

World Bank. 2019. Green Bond Impact Report 2019. Washington, DC: The World Bank, November 2019. Available fromhttp://pubdocs.worldbank.org/en/790081576615720375/IBRD-Green-Bond-Impact-Report-FY-2019.pdf.

World Bank. 2020a. “IBRD Funding Program: Sustainable Development, Bonds.” The World Bank Group, 2020. Available from https://treasury.worldbank.org/en/about/unit/treasury/ibrd#1.

World Bank. 2020b. Bonds for Sustainable Development: Impact Report 2019. The World Bank Group, 2020. Available from http://pubdocs.worldbank.org/en/138051589440217749/World-Bank-Sustainable-Development-Bond-Impact-Report-2019.pdf.

WRI (World Resources Institute). 2019. “So Far, Green Bonds Fail to Raise Much Money for Resilience. The Climate Resilience Principles Aim to Change That,” by G. Larsen, G. Christianson, and N. Amerasinghe. WRI, October 15, 2019. Available from https://www.wri.org/blog/2019/10/so-far-green-bonds-fail-raise-much-money-resilience-climate-resilience-principles-aim.

Zhang, H. 2020. Regulating Green Bond in China: Definition Divergence and Implications for Policy Making. Journal of Sustainable Finance and Investment 10(2): 141–156. Available from https://doi.org/10.1080/20430795.2019.1706310.