Does a Higher Degree and Higher Cost of Leverage Worsen Corporate Environmental Performance?

2,429

The increasing global focus on environmental investments raises concern about the relationship between a firm’s cost of capital and its corporate environmental (ESG) performance. However,…

Micol Alexandria Chiesa, PhD

Lecturer

Lecturer in Circular Economy at Oxford University, School of Geography and the Environment Oxford, University Centre for the Environment

Suborna Barua, PhD

Associate Professor

Associate Professor at the Department of International Business, University of Dhaka

Abstract

The increasing global focus on environmental investments raises concern about the relationship between a firm’s cost of capital and its corporate environmental (ESG) performance. However, there is little research on the topic. The previous literature on corporate finance has found that capital constraints play a role in companies’ investment decisions. This article contributes to the existing corporate finance literature by looking at the impact of the cost of corporate debt and the degree of leverage on corporate environmental performance (CEP). We use a cross-section regression framework incorporating four key explanatory variables in addition to other control variables (capital structure, the total cost of debt (COD), cost of long-term debt, and cost of short-term debt) to examine the effects of the cost of debt and the degree of leverage on CEP for selected publicly listed corporations from the United States, the United Kingdom, Australia, and Canada. We use the environmental pillar score from Thomson Reuters ESG data to measure the CEP. The literature identifies debt financing as an important resource for helping organizations implement their strategies, particularly environmental ones. However, the findings suggest that a prospective higher cost of debt may cause firms to deviate from their environmental objectives, thus achieving lower CEP.

1. Introduction: Does a Higher Degree and Higher Cost of Leverage Worsen Corporate Environmental Performance?

The acceleration of climate change in recent years has increased the pressure on corporations to improve their environmental practices, and key stakeholders expect to see an increased level of corporate environmental accountability (Buysse and Verbeke 2003; Delmas and Toffel 2008; Kassinis and Vafeas 2006). Corporate environmental performance (CEP) across company value chains presents great opportunities but comes with substantial costs (Economist Intelligence Unit 2008). Earlier examinations find that capital constraints assume critical roles in strategic decision making by influencing the firm’s major investment decisions (Ducassy 2013; Stein 2003). The direct or indirect pressure for sustainability actions, either mandatory or voluntary, may require budgetary allocations or commitments that corporations either cannot afford or may fail to prioritize over financial returns. Therefore, sustainability concerns, like any other corporate action, require sufficient external or internal incentives.

Scholarly attention and managerial practices have made CEP a critical performance metric for corporations in recent years. This is particularly evident in the attempts of a growing body of literature to link CEP and corporate outcomes from different vantage points (such as those of investors and lenders). Lenders view companies with poor environmental records as risky investments, and compared with their better performing counterparts, more readily exposed to a higher risk of litigation. According to Derwall et al. (2011), exposure to higher risk drives lenders to demand higher interest rates for financing the debts of companies with poor environmental records. Earlier studies on environmental performance focused on the relationship between the CEP and financial performance of corporations from a lender’s point of view (Dixon-Fowler et al. 2013; Endrikat et al. 2014). However, although there is little clarity over how lenders perceive the corporate cost of meeting higher environmental performance, it is evident that the cost of raising funding to pay for the strategies necessary to increase this performance may be a barrier, as it is based on the market mechanism that guides the issuance of debt capital for environment-friendly investments (Luo et al. 2015). Regardless of whether CEP can explain, or is explained by, financial performance, neither the literature nor practitioners are adequately addressing the question of how the cost and structure of capital are influencing CEP.

The focus of this chapter is on how the cost of the corporate debt and capital structure (that is, the degree of leverage) influences CEP. Debt financing has an important effect on how an organization implements its strategies, including environmental ones. However, a higher degree of leverage and/or a higher cost of debt could lead firms to deviate from their environmental objectives and prevent CEP. The urge to generate higher financial returns to service a debt could drive such a deviation. To examine the effects of the cost and degree of leverage on CEP, in addition to the other control variables, four key explanatory variables are considered – capital structure, total cost of debt, cost of long-term debt, and cost of short-term debt. To capture CEP, the environmental pillar score from Thomson Reuters ESG data is used for selected publicly listed corporations from the United States, the United Kingdom, Canada, and Australia. The effects are estimated at three levels: (i) all companies as a whole; (ii) country-specific separate assessments; and (iii) sector/industry-wide estimations. Section 2 contains a review of the literature and an outline of the hypotheses to be tested; section 3 details the methodology followed; section 4 presents and discusses the results; and section 5 follows with a conclusion and a discussion about the implications of the findings.

2. Review of the Literature and Hypotheses

This section covers the definition and measurement of CEP, general determinants of CEP, the link between degree of leverage and CEP, and the link between COD and CEP.

Definition and Measurement of CEP

Over the last couple of decades, CEP has become a prominent field of research, and several authors have tried to deliver a standard definition of it (Dahlsrud 2008; Poser et al. 2012; Trumpp et al. 2015), but there is still no agreed upon version (Yang Spencer et al. 2013). A key reason for this is that environmental issues cross complex fields of design, manufacturing, marketing, social responsibility, employees, and the public at large (Etzion 2007).

Scholars across a wide range of research areas and disciplines have focused on the construct of CEP and examined its relationship with different organizational constructs or variables. Hart (1995) defines environmental performance as a combined approach of product stewardship, pollution prevention, and sustainable use of resources.

A large body of literature suggests measuring environmental performance in terms of environmental impacts and outputs, such as toxic emissions/pollution (Cormier and Magnan 1997; Khanna and Damon 1999; Patten 2002; Sam et al. 2009), emission volume (Porter and van der Linde 1995), ratio of emission over output level (Arimura et al. 2008; Earnhart and Lizal 2007), and emission intensity (Jiang et al. 2014).

CEP can also be indirectly measured by the degree of compliances to environmental regulations (Dasgupta et al. 2000; Gangadharan 2006), chemical waste/recycled waste (Al-Tuwaijri et al. 2004; King et al. 2005; Theyel 2000), product life management score and ISO 14001 certifications (Lefebvre et al. 2003), level of energy usage (Cole et al. 2008), self-report surveys from managers (Judge and Douglas 1998; Dixon-Fowler et al. 2012), and a firm’s emission reduction (Barba-Sánchez and Atienza-Sahuquillo 2016). Henri and Journeault (2010) argue that these “single component-focused” approaches limit the scope of environmental performance to operational outcomes and fail to consider further strategic elements of the construct (for example, product innovations or resource use).

Stakeholders are increasingly recognizing the importance of CEP and empirical studies show that analysts are considering environmental performance in their research recommendations (Ali 2017; Clark and Viehs 2014; Dahlsrud 2008; Eccles et al. 2011; Ioannou and Serafeim 2015). Particularly for large firms, greater environmental disclosure is found to be associated with an increase in analyst forecast accuracy (Dhaliwal et al. 2012). In this regard, many global corporations are paying increased attention to their environmental performance and, thus, increasing their resource allocations to environmentally friendly investments. Given that risk management is a key driver in superior economic performance (Oikonomou et al. 2014), companies are increasingly considering sustainability strategies to circumvent various risks, particularly any that might spoil their reputation.

In this research, CEP is measured in terms of the cumulative environmental pillar score measured by Thomson Reuters ESG database, which consists of weighted averages of three specific scores—resource use, product innovation, and emission reduction; this measurement is consistent with Hart’s (1995) definition.

General Determinants of CEP

The available literature identifies a wide range of factors that affect CEP. Many empirical studies employ theoretical arguments to define the components and underlying features of CEP, particularly stakeholder theory (Brammer and Millington 2008; Donaldson and Preston 1995; Freeman 2010; Jones 1995; Mitchell et al. 1997; Orlitzky et al. 2003) and resources dependency theory (Berman et al. 1999; Branco and Rodrigues 2006; Hillman and Keim 2001; McWilliams and Siegel 2001; Russo and Fouts 1997). González-Benito and González-Benito (2006) identify three features that often drive the environmental proactivity of firms: these are (i) company-specific factors (such as size and degree of internationalization), (ii) stakeholder pressure (primary-secondary, internal-external), and (iii) external factors (like location and sector of operation).

An environmental management system in a firm generally consists of internal policies, assessments, and the implementation of actions that affect the entire enterprise and its relationship with the natural environment. Institutional theory suggests that regulatory, market and social pressures could constrain an organization’s economic activities and/or create opportunities for strategic advantage with respect to the firm’s environmental interactions (Hoffman 1999). As customers become increasingly aware of the natural environment, market pressures may encourage companies to engage in proactive environmental strategies (Darnall et al. 2005). Hoffman (1999) and King and Lenox (2000) found that environmental accidents have significantly increased social pressure from environmental and social groups, as well as from the relevant trade associations and labor unions.

The Link between Degree of Leverage and CEP

The level of debt in a capital structure, that is the degree of leverage in a firm, is a significant determinant of the strategic choices made in an organization’s financial management. An optimal debt level in the capital structure is a critical prerequisite for any business wanting to achieve sustained profitability, firm value, and an increased ability to deal with market competition (Yazdanfar and Öhman 2015). According to Jensen (1986), if ownership and management are separated, as they usually are in large companies, debt financing has a disciplinary effect in that it increases the pressure on managers to perform more efficiently.

According to Magnanelli and Izzo (2017), when making issuance of debt decisions, lenders are likely to consider the post-cost-benefit trade-off, which might include the expectations of future compensations for environmental investments. These considerations fall broadly in line with stakeholder theory (Miles 2017).

The relationship between the financing structure and a firm’s performance is a frequently discussed topic in managerial finance. The presence of debt, either long or short term, in the balance sheet entails a periodic fixed cost in the form of financial expenses. A higher degree of leverage would mean higher repayment burdens over the term or maturity of the debt; such burdens, particularly of higher long-term debt, could significantly constrain a firm’s operating and investing abilities over a longer time period. In such cases, to meet higher repayment burdens, firms might be forced to prioritize financial returns over anything else, such as environmental concerns, and use up some of the funds reserved for their corporate social responsibility (CSR) activities. Furthermore, firms might also decide to cut back some of their costs that do not provide immediate financial benefits, such as waste recycling, emission level reduction, and environmental resource efficiency. These consequences are eventually likely to reduce the CEP of firms. Schneider (2011) argues that poor CEP puts a firm at risk of future clean up and compliance costs, which may threaten the polluting firm’s ability to pay creditors in the long term.

The prioritization of financial returns over environmental commitment could become more serious particularly in periods of economic downturn. Pruitt and Gitman (1991) found that firms with a higher degree of leverage experience a higher volatility in investment and expenditure. In such a situation, managers lack strong incentives to invest in the environment and are likely to divert the debt capital to other profitable investments with higher short-term returns. To reduce the volatility, the firm’s investment portfolio can be altered to sectors that provide higher rates of return but that generate higher environmental cost; such sectors could include coal and ore mining, cow ranching, or nonrenewable energy development. The inclinations toward financial returns over environmental performance could be further motivated by weak regulations and lack of incentives. Overall, the deviation from environmental toward financial objectives is likely to lower a firm’s CEP.

The Link between COD and CEP

The cost of a firm’s capital originates from the cost of equity and debt utilized in its capital structure. Several studies suggest that CEP could have a significant association with COD. Ng and Rezaee (2015) found that firms engaging in environmental misconducts evoke negative reactions from lenders because such behavior is likely to affect the firm’s default risk. This in turn could raise the cost of further financing for those firms. In other words, a firm’s cost of debt could be prone to corporate social responsibility externalities. In an effort to negate lender reactions, firms often tend to publish information on their environmental performances. Kaymak and Bektas (2017) find that firms often produce useful environmental information for lenders, and more environmental disclosures tend to help lower the cost of capital removing the information asymmetry (Dhaliwal et al. 2011). Corporations are thus keen to leverage their environmental performance, which Martínez and Frías (2015) see as a way of reducing the cost of debt capital. In a study of the relationship between CEP and cost of debt, Eichholtz et al. (2019) point out that the cost of debt for commercial mortgages and corporate debt of property companies (REITs) is also affected by “the crisis and post crisis period,” especially in the post crisis period, since lenders increasingly include environmental deliberations when determining their loan pricing.

Firms with poor CEP are more likely to risk litigation and clean-up costs, which could reduce their debt repayment abilities (Schneider 2011; Tse 2011). Lenders therefore charge more interests to companies that present poor CEP. Bauer and Hann (2010) find that companies with better environmental management have lower loan spreads, while Chava (2014) argues that firms with several pending environmental issues are likely to face significantly higher interest rates on their loans. Other studies suggest that companies that behave irresponsibly in relation to environmental, social, and governance (ESG) standards are likely to incur fines, penalties, government sanctions and other associated litigation costs, which in turn could result in a higher cost of capital financing and restrict access to finance (Bauer and Hann 2010; Dhaliwal at al. 2011). Companies with good CEP records tend to be better placed to minimize risk (Chen et al. 2018). According to Yazdanfar and Öhman (2015), such risks are associated with an increase in debt covenants as the environmental performance of a company decreases (El Ghoul et al. 2011; Hong and Kacperczyk 2009). Oikonomou et al. (2014) and Bauer and Hann (2010) show that firms with better corporate environmental management enjoy a lower cost of debt financing, and recent studies provide further support for this relationship (Erragragui 2018; Fonseka et al. 2019; Jung et al. 2018).

Many studies suggest that firms with socially responsible and environmentally sustainable practices have a significantly lower cost of equity (Borghesi et al. 2014; Crifo and Forget 2015; Dhaliwal et al. 2011; El Ghoul et al. 2011; Mackey et al. 2007; Sharfman and Fernando 2008). Harrison and Wicks (2013) use agency theory to explain the conflicting interests between the shareholders and managers of corporations engaged in sustainable investments. They believe that shareholders expect managers to invest adequately in environment-friendly activities and projects to ensure that they are more stable and able to sustain themselves in the long term. Also, shareholders (owners) expect managers (agents) to deliver optimal returns and to ensure that there is an adequate cash flow to pay off debts and the interest on them over time (Engle 2007; Walls et al. 2012).

However, being environmentally responsible might interact with firms’ operation performances. Several studies note a significant relationship between CEP and corporate performance, though they return different verdicts (Albertini 2013; Endrikat et al. 2014; García‐Sánchez and García‐Meca 2017; Hang et al. 2019; Herremans et al. 1993; Porter and Kramer 2006; Trumpp and Guenther 2017; Venturelli et al. 2018; Wiseman 1982). Goss and Roberts (2011), on the other hand, argue that some environmental investments tend to be very costly and might lower the company’s profitability in the short run, though they find the returns in the long run to be unclear. Recent trends suggest that in an effort to leverage environmentally friendly strategies in raising capital at an attractive cost, firms are increasingly considering using sustainable borrowing sources, such as green bonds (Barua and Chiesa 2019; Chiesa and Barua 2019). In this regard, corporations with good environmental credentials are likely to attract lenders and therefore lower the cost of debt.

Several studies have found a negative association between the cost of capital and financial and market performance (Gebhardt et al. 2001; Gode and Mohanram 2003; Lambert et al. 2012), which could also relate to a firm’s environmental performance. Cost of debt capital could influence CEP, for Harrison and Wicks (2013) argue that the tendency of managers to pursue short-term objectives to lower their cost of debt could drive their decision and attention to divert away from environmental performances.

The literature on the link between COD and CEP does not offer much knowledge on how COD could influence the CEP of firms, although such an understanding is critical to placing appropriate mechanisms that could make corporations behave more responsibly. For example, if a higher cost of long-term debt forces firms to prioritize financial benefits over environmental concerns (in order to repay the debt over a long period of time), it would eventually reduce the firms’ environmental performance. Such a likelihood could also be evident across firms (for example, firms experiencing higher costs could have lower CEP). While the pressure of debt financing to a greater extent or to a higher cost could force firms to deviate significantly from environmental concerns, a lower degree of leverage or a lower cost of debt financing could also allow them to include environmental considerations in business and investment decisions. However, as specified before, no empirical study in the existing literature, to the best of my knowledge, has studied the potential effects of COD and the degree of leverage on CEP. In this article, I address this research gap by testing the following hypotheses:

Hypothesis 1. Cost of total debt does not influence CEP.

Hypothesis 2. Cost of long-term debt does not influence CEP.

Hypothesis 3. Cost of short-term debt does not influence CEP.

Hypothesis 4. Degree of leverage, which is capital structure, does not influence CEP.

3. Data and Methods

In this section, I detail the methodology of empirically testing the above hypotheses.

Variables and Model Specification

The exploration of the effects of the cost of debt and capital structure (namely the degree of leverage) on the environmental pillar (EP) score starts with the following functional relationship:

Where,  is the environment pillar score,

is the environment pillar score,  denotes constant,

denotes constant,  is the cost of debt,

is the cost of debt,  stands for capital structure,

stands for capital structure,  denotes control variables,

denotes control variables,  indicates the number of vector, and

indicates the number of vector, and  is the error term. The intention is to examine the effects of the costs of long-term and short-term debt separately. Therefore, equation (1) can be expanded as follows by breaking down the cost of debt into the cost of short-term debt

is the error term. The intention is to examine the effects of the costs of long-term and short-term debt separately. Therefore, equation (1) can be expanded as follows by breaking down the cost of debt into the cost of short-term debt  and the cost of long-term debt

and the cost of long-term debt  ):

):

From the literature and available data, it is possible to identify a set of control variables. These are firm size, business growth, market risk, age and experience, profitability, capital investment, and cash flow. To operationalize equations (1) and (2), capital structure is captured by debt-equity ratio (DEQ), firm size by total assets (TA), business growth by revenue growth (GR) market risk by firm beta (Beta), age and experience by age of business (Age), profitability by return on assets (ROA), capital investment by annual capital expenditure (CAPEX), and cash flow by operating cash flow (OCF). Therefore, equations (1) and (2) can be expanded as follows for final estimations:

In addition to the variables defined, equations (3) and (4) also control for country fixed-effects (C) and industry/sector (S) fixed-effects. A detailed definition of all variables specified in equations (3) and (4), alongside the justifications for their inclusions and their expected impacts, is discussed below.

In this analysis all the corresponding dependent variables are taken at the same point in time (t0) while CEP is taken at t+1. This is because corporate strategic decisions, particularly project financing for environmental projects, may be reflected on the score accounted the year after.

Corporate Environmental Performance. This is measured CEP by using the Eikon ESG environmental pillar (EP). Following the definition provided by Eikon, the environmental pillar consists of the weighted average of three specific scores—resource use (32.35%), product innovation (32.35%), and emission reduction (35.30%). These criteria are in line with Hart’s (1995) definition of environmental performance.

Thomson Reuters ESG scores are transparent, objective measures of the relative ESG performances of different companies with a weighted structure that guarantees the information is consistent and comparable across sources and companies.

Using company-reported data, the scores also capture the commitment and success of a company in addressing important environmental themes. Thomson Reuters ESG scores, presented as either a percentage or as a letter grade, are simple to understand. According to Cho et al. (2013), they provide the best source of intelligent information, which is widely used by businesses and professionals alike. This is because Thomson Reuters ESG data are based on more than 250 key performance indicators and original data sources. Trained research analysts collect the data from a variety of sources, including but not limited to company reports, stock exchange filings and news agencies. After gathering the material, the analysts convert the qualitative data into easier-to-understand quantitative data units. Thus, professional and experienced evaluators achieve consistent and transparent Thomson Reuters scores. For this study, the cost of debt is a representation of the lender’s marginal cost. It is the sum of the weighted costs of short- and long-term debt based on the one- and ten-year points of an appropriate credit curve. In the three selected countries, Thomson Reuters ESG scores applied indices of different levels of importance based on industry-specific, country-specific, and regional operations.

The resource-use score reflects a company’s performance, as well as its capacity to reduce the use of materials, energy, or water, and to find more eco-efficient solutions by improving supply-chain management. The innovation score reflects a company’s capacity to reduce environmental costs and burdens on its customers by creating new market opportunities through the adoption of new environmental technologies and processes, or through eco-designed products. The emission reduction score measures a company’s commitment to and success in reducing environmental emissions in its production and operational procedures.

Cost of Debt. The cost of debt represents the marginal cost to the company of issuing a new debt. It is calculated by adding the weighted cost of the short-term debt and the weighted cost of the long-term debt based on the one- and ten-year points of an appropriate credit curve. The costs of the short- and long-term debts are the marginal costs to the company of issuing new short- and long-term debts, respectively.

Capital Structure. The capital structure (or debt-equity ratio) is the proportion of debt and equity under a firm’s control. In other words, it indicates the amount of leverage used in the firm’s total capital investment. This is in line with Jensen and Meckling’s (1976) argument that stringent debt covenants associated with the use of debt might confine a manager’s ability to operate freely, which in turn affects the firm’s performance. Moreover, the use of debt may decrease a manager’s share of equity and mitigate the loss that arises due to conflicts between managers and shareholders (Harris and Raviv 1991). The debt-equity ratio (DEQ) is used as a measure of capital structure and is expected to have a negative relationship with the EP.

Control Variables. In addition to the key variables detailed above, several measures commonly used as controls in the analysis of financial performance are included (Berger and Ofek 1995). The size of the firms (Size) is controlled because size affects the issuing of environmental reports, especially when large firms face pressure from the public or have adequate financial resources (Lang and Lundholm 1993). Size is also controlled because, generally, larger firms are considered safer and less risky than smaller ones. Firm size can be measured using some proxies, such as total assets, sales, and number of employees (Berger and Di Patti 2006; Majumdar and Chhibber 1999; Sheikh and Wang 2011). Firm size is measured as the natural logarithm of total assets (lnTA) and is expected to be positively associated with CEP.

The proxy variable for firm age (Age) is the number of years since the firm’s date of incorporation. Older firms are a priori more likely to benefit from a longer history of reporting (learning advantage), business experience, and more substantial pressure from investors and peers. Age is expected to be positively related to CEP.

There is also a control for a firm’s growth rates (Growth) and this is compared with the three-year compound annual growth rate (CAGR) of EBITDA. The control for growth opportunities is necessary because, in an expansionary period, firms are more financially constrained and have fewer resources for environmental activities and disclosure. However, growing firms also tend to have higher levels of information asymmetry, which could encourage managers to make more disclosures to attract potential investors (Dhaliwal et al. 2011; Giannarakis et al. 2018). Growth is expected to be negatively related to CEP.

CEP often interacts with capital markets and investors. To capture the market reaction and risk, the firms’ three-year monthly beta coefficient is used. Beta is the measure of movements in the firm’s stock price in response to the movements in the broad market index. Thus, it captures market and investor reactions to corporate actions and, as the literature shows, market and investor reactions often guide corporate actions. Hence, market and investor reactions primarily drive beta controls for the changes in the EP due to corporate actions. Although it is difficult to anticipate a direction, there is a naïve expectation that it will be positively related to CEP; that is, a higher market risk would possibly drive companies to become more environmentally responsible.

Return on assets (ROA) captures the influence of financial performance on CEP. As employed in previous studies (Margolis et al. 2003), ROA is a standard accounting measure of financial performance commonly found in strategy research. There could be a positive association between financial performance and the EP, for higher profitability would give firms more financial resources for reinvestment. However, a negative association could emerge if, by prioritizing financial incentives over environmental concerns, firms sacrificed environmental performance in favor of higher profitability.

Capital expenditure (CAPEX) denotes the funds a company uses to acquire, upgrade, and maintain physical assets such as property, industrial buildings, and equipment. CAPEX is measured as the natural logarithm of capital expenditure (lnCAPEX). As firms often use CAPEX to embark on new projects or investments, the expectation is that this type of financial outlay will affect environmental performance negatively, except when companies make investments to maintain or increase the sustainability of their operations.

The operating cash flow (OCF) is used to capture the firm’s financial performance, its strength, and the availability of its liquid resources. Firms that can produce a higher level of cash flow from their operations can also generate greater financial returns from their regular business. Firms that generate higher OCF are generally regarded as having better financial health. In addition, a higher OCF means that more liquid financial resources are available to reinvest in the firm, including environmental resources. Therefore, greater cash generating firms are likely to be able to commit more resources to environmental concerns, which would yield a better CEP. The research uses natural log converted OCF values (lnOCF) and a positive association between the OCF and CEP is expected.

In addition to the control variables identified above, the economic sector/industry fixed-effects (S) and the country fixed-effects (C) are included to control for fixed regulatory, economic, and market-factor differences (for example, demand, supply, and prices) and the cyclical nature and average capital intensity of the industries under consideration.

Data

In estimating the cross-section equations (3) and (4), data are extracted on firms with ESG information from Thomson Reuters (TR) available through Eikon, which covers 3,507 companies headquartered in the United States, the United Kingdom, Canada, and Australia. The environmental pillar (EP) score from the ESG framework is used to measure corporate environmental performance (CEP). The 2017 score values of the EP and the 2016 values for all the explanatory variables for all the firms are considered. This is because, to be reflected in the firms’ EP scores, one would expect any effect of the explanatory variables considered to require a time lag. This time lag is considered to be one year, meaning that the effects of the explanatory variables on the EP score is considered after this time. The data are collected from Thomson Reuters to ensure that the information is standardized, comparable and reliable. All the ESG data are quality controlled and verified in a rigorous process to remove potential errors. Considering the cross-section data gathered, ordinary least squares (OLS) regressions are used to estimate the equations (3) and (4). (For more information on the definition of each industry please refer to Table 3.)

The distribution of companies available in the data across the four countries and the Thomson Reuters Business Classification (TRBC) sectors/industries shows that the data are heavily led by the United States (Table 1). About 70% of the companies are headquartered there, followed by the United Kingdom, Australia, and Canada. Given the distribution of the samples, a three-phase approach is adopted toward estimating equations (3) and (4). First, both equations are estimated for the whole sample combining all companies. Second, country-wide estimations of the equations are carried out for the four countries separately. Finally, sector/industry-wide estimations are run for both equations for the ten sectors/industries separately. However, considering the adequacy of the sample size, only run sector/industry-wide estimations are run for the United States.

Table 1: Sample Breakdown by Country and Sector/Industry

| Name | Australia | Canada | UK | USA | Total |

| Basic materials | 91 | 72 | 30 | 129 | 322 |

| Consumer cyclicals | 52 | 29 | 78 | 356 | 515 |

| Consumer noncyclicals | 29 | 10 | 25 | 119 | 183 |

| Energy | 35 | 67 | 20 | 145 | 267 |

| Financials | 71 | 54 | 118 | 581 | 824 |

| Healthcare | 23 | 9 | 22 | 338 | 392 |

| Industrials | 47 | 30 | 75 | 342 | 494 |

| Technology | 20 | 14 | 17 | 315 | 366 |

| Telecommunications services | 5 | 6 | 5 | 27 | 43 |

| Utilities | 8 | 14 | 9 | 70 | 101 |

| Total | 381 | 305 | 399 | 2422 | 3507 |

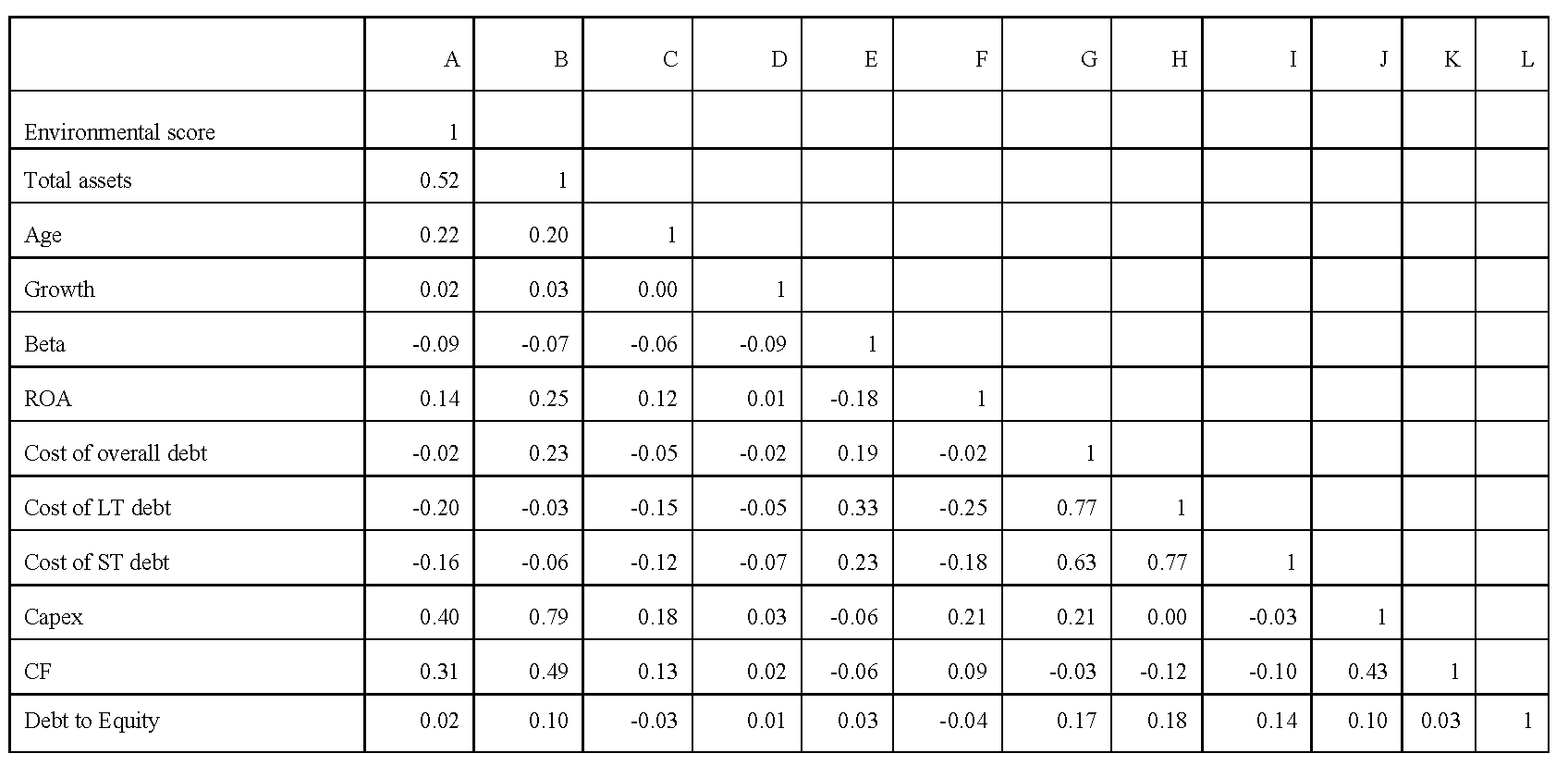

Table 2 contains the descriptive statistics for the variables of the whole sample, including those for country and sector/industry, which show the broad characteristics of the data. Two common challenges involved in cross-section OLS estimations are multicollinearity and heteroskedasticity. To identify the potential biases, Breusch-Pagan/Cook-Weisberg and variance inflation factor (VIF) tests are run to detect heteroskedasticity and multicollinearity, respectively.

Table 2: Correlation Matrix

Source: Authors’ calculations.

Since Table 1 shows that some estimation samples display heteroskedasticity, robust estimations for them are carried out to minimize the biases. Two sectors—the US sectoral samples of telecommunication and utilities—show significant multicollinearity mainly due to the very small sample size. In the detailed VIF estimates, the OCF variable is found to contribute greatly to multicollinearity, and, therefore, for these two sectors the equations are estimated after removing the OCF variable. All other samples, following the mean VIF cut-off value of ten (O’Brien 2007), show no significant multicollinearity. Table 2 shows the correlation matrix among the variables, which further supports the VIF results.

4. Results and Discussion

Table 3 reports the results of the estimations of equations (3) and (4) for all firms included in the sample. Although the research began with a dataset on a total of 3,507 firms, given the data availability of different variables considered, the estimations procedurally included a maximum of 2,147 firms. The estimations controlled for both sectoral and country fixed effects.

Cost of Debt

The estimates for equation (3) in Table 3 show that the cost of the total debt has a negative effect on a firm’s environmental performance (CEP) and the result is significant at a 1% level. The results suggest that a 1% increase in the overall cost of a debt in a year (2016) is associated with a reduction of EP. Estimates suggest that a lower cost of debt increases environmental performance the following year (2017). This is further confirmed by the results of equation (4) on the separated effects of the costs (long and short) which have significant and negative effect on CEP. The result is significant at 1% level. The results suggest that a 1% increase in the cost of a long-term debt in a year results in a decrease in environmental performance (CEP) by a score of 2.00 in the following year. This result indicates that the higher the cost of a firm’s long-term borrowing, the lower its environmental performance is likely to be. However, this appears to be the opposite for the costs of short-term debt. The cost of a short-term debt shows a positive effect on CEP, and it is significant at a 5% level; a 1% increase in the cost of a short-term debt in a year is associated with a corresponding increase in CEP by a score of 1.54 in the following year.

The estimates could mean that long-term debt tends to be more expensive, possibly because of the greater uncertainty involved; it is likely to discourage corporations from making financial commitments to environmental investments. According to Palley (2013), a large long-term debt has the potential to create higher financial obligations, which may encourage managers to divert debts meant for environmental investments into alternative, more profitable, investments. In addition, since environmental performance has no short-term financial payoff, or cannot be translated into short-term financial returns, environmental investments may receive less consideration. This factor could be driving lower environmental performance.

Table 3: Effects of Cost of Debt on EP: All Sample (equations 3 and 4)

| Variables | Equation (3) | Equation (4) |

| Firm Size (lntot_assets) | 6.373*** (0.588) | 6.446*** (0.585) |

| Age | 0.094*** (0.014) | 0.088*** (0.014) |

| Growth | -0.604 (0.498) | -0.596 (0.502) |

| Beta | 0.373 (0.660) | 0.823 (0.676) |

| ROA | 0.056* (0.032) | 0.037 (0.034) |

| CF (lnOCF) | 1.146** (0.511) | 0.922* (0.523) |

| COD | -1.053*** (0.254) | – |

| COLTD | – | -2.002*** (0.370) |

| COSTD | – | 1.542** (0.660) |

| CAPEX (lncapex) | 0.676** (0.344) | 0.632* (0.345) |

| Leverage (Debt to Equity) | -0.000 (0.000) | 0.000 (0.000) |

| Constant | -118.059*** (5.197) | -112.427*** (5.326) |

| R-squared | 0.392 | 0.397 |

| Prob>F | 0.000 | 0.000 |

| No. of obs. | 2,147 | 2,146 |

| Sector-FE | Yes | Yes |

| Country-FE | Yes | Yes |

| Multicollinearity [VIF test statistic] | 2.30 | 2.46 |

| Heteroskedasticity (Chi2 statistic) [Breusch-Pagan / Cook-Weisberg test] | 7.46*** | 7.61*** |

Source: Authors’ calculations.

The positive effect of the cost of short-term debt, however, offers a different insight. Generally, environmental performance requires time to reflect and a commitment to long-term funding. Firms only take out short-term loans to invest in the environment if they urgently need to improve their credentials to impress their stakeholders and stockholders (Clark et al. 2015). However, short-term borrowing can be used for environmental purposes, such as taking advantage of a premium price for more sustainable inputs, or paying off environment-related fees, charges, or lawsuits. In such cases, a firm could be incentivized to borrow short-term, even if it carries a higher cost.

All in all, the findings suggest that greater long-term obligations and higher long-term costs can reduce corporate environmental investments and therefore influence environmental performance. Firms may be motivated toward short-term investment to drive immediate environmental performance. A higher cost of short-term debt creates an obligation for a shorter period only; a desire to appear more responsible to the stakeholders in the short run could encourage firms to borrow at a higher rate.

Capital Structure

The estimates of both equations confirm no statistically significant effect of degree of leverage on CEP. The results indicate that higher debt equity does not necessarily affect CEP, in particular, negatively.

Considering the effects of both cost of debt and capital structure, the overall results indicate that it is the cost, not the degree of leverage, that significantly affects CEP. The ability of corporations to gain profit, indicated by the degree of leverage, has little effect on CEP. By contrast, the cost of debt determines how a loan can increase profits and, in turn, the amount of resources available for CEP.

Control Variables

For the estimates, the most important control variables were selected from the literature. According to the estimates for both equations, firm size (total assets) has a significant positive effect on CEP. According to the estimates of equations (3) and (4), a 1% increase in total assets in a year is associated with a corresponding rise of CEP by a large score of 6.373 and 6.446, respectively. These results indicate that the environmental performances of larger firms are likely to be better than those of their smaller counterparts. Furthermore, the estimates for both equations show that the age of a firm has a significant positive effect on it; according to equations (3) and (4), an extra year in age is associated with an increase in CEP by a score of around 0.09. This result could indicate that older firms are likely to perform better environmentally. This is consistent with earlier studies indicating that older firms, having potentially been in the market for a longer period of time and with greater experience, are likely to be more environmentally responsible. This result is not surprising. Given that they have access to more resources, larger firms are often at a more advanced stage of addressing environmental issues and, for many years, are likely to have incorporated environmental management into their environmental strategy.

Furthermore, larger firms often have more knowledge of how to deal with multiple stakeholder pressures; and, due to their longer experience, they have also been able to acquire the resources and skills they need to engage with the environmental activities of their business. An explanation for the import of firm size is that it can be used to reflect firm visibility, and since larger firms tend to be more susceptible to public scrutiny, they are more likely to be industry leaders on environmental performance.

Additionally, there is a significant positive effect of return on assets on environmental performance, as evidenced by the equation (3) estimates. The results suggest that a 1% increase in ROA in a year is associated with a corresponding increase in the CEP score by 0.06 points in the following year (in this case 2017). This result show that firms with a higher profitability are likely to have a better environmental performance. Profitability variables like ROA and ROS (return on sales) have an impact on CEP. The findings echo those of Qi et al. (2014) who found that a firm’s financial performance affected its environmental performance.

The estimates of both equations consistently indicated a significant positive effect of operating cash flow (CF) on CEP. Those of equations (3) and (4) suggest that an annual increase of the EP score by 1.15 and 0.92 points respectively is associated with a 1% increase in operating cash flow in the preceding year. These estimates suggest that firms with a higher operating cash flow are likely to have a better environmental record. Firms with a higher operating cash flow have a greater potential for growth and therefore higher value price. According to Dragomir (2010), corporations with higher value price tend to have better environmental performances. No significant effect of firm growth on CEP is found. An intuitive argument is that companies grow faster because they invest more in return-generating business opportunities to fulfill corporate objectives like expanding their production capacity or opening a new product line, but not because they invest in environmental practices or sustainability. Hence, growth may not have a relationship with CEP. However, although insignificant, the coefficients of the growth variable show a negative sign across the estimations, indicating a likely negative effect. A negative effect is likely when firms sacrifice environmental concerns to achieve a higher business growth, guided by purely business motives. Like growth, the other control variable, market risk, also shows no significant effect on the environmental performance of firms. It therefore confirms that corporate actions on the EP are not a response to the investor reactions or market movement in the stock prices. In other words, corporations do not factor in market reactions or movements while considering environmental issues in their business decision-making.

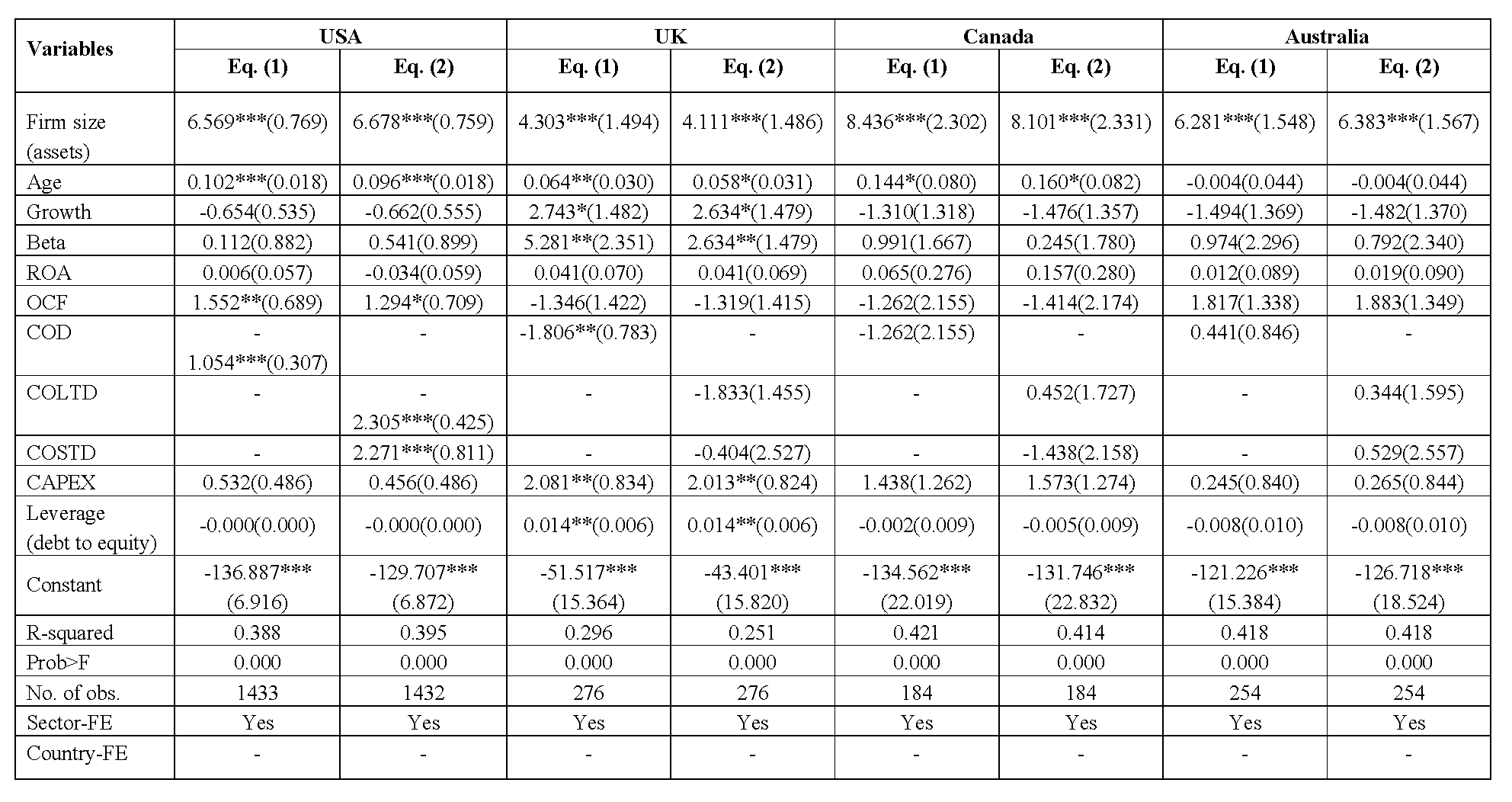

Country-Level Investigation

When analyzing the data at a country level, the results appear highly heterogenous (Table 4). The significant and negative effects of the cost of the total debt (equation 3) on CEP can only be confirmed for the United States and the United Kingdom. Estimates for these countries are broadly consistent with all the sample estimations explained earlier; CEP declines by an annual score of 1.55 for the United States and 1.81 for the United Kingdom due to a 1% increase in the overall cost of the debt in the previous year. However, when the cost of the debt is broken down (equation 4), the negative and positive effects of the cost of long-term and short-term debt respectively can only be confirmed for the United States. Consistent with all the sample effects observed earlier, a 1% increase in the annual cost of long-term debt is associated with a corresponding decrease in CEP by a score of 2.31 for the US points. A similar increase in the cost of a short-term debt is associated with an increase in CEP by a score of 2.27 points. However, the breakdown estimates (equation 4) suggest that cost has no significant effect on either long- or short-term debt for the United Kingdom and no significant effect on any of the cost of debt variables for Australia and Canada.

In the last three years alone, environmental, social, and governance (ESG)-related regulations have doubled across the United Kingdom, the United States, and Canada, which suggests that the ESG regulatory landscape is evolving fast (Datamaran 2018). While there are more discussions about CEP in the United States and the United Kingdom, the long-term lending interest rates in these two countries over the last decade have been the second and third highest among the four in question. A possible link between the two countries in this respect is that, faced with a higher lending rate, firms perhaps fail to improve rather than lower their CEP standards. This result is consistent with the argument presented earlier that firms with a higher cost of debt, particularly long-term debt, are likely to bear the extra burden of having to secure the ability to repay it. That a significant portion of its income is being used for high-cost debt servicing would limit a firm’s ability to pledge funds for environmental purposes. In such situations, corporations generally prioritize their finances over the environment.

Table 4: Country-wise Effects of Cost of Debt on Environmental Performance (equations 3 and 4)

Source: Author’s calculations.

In Canada and Australia, a lack of significance can be explained by the real nature of the level of compliance. In Australia, despite increased debate on environmental regulations and their enforcements, poor CEP, whether intentional or unintentional, has become increasingly evident in recent years. Mineral-based extractive industries in Australia, such as coal, are very important for the economy. In the last decade, despite pressure from several green groups and community organizations, the country actually increased its reliance on pollutants. For example, while coal is considered the worst of the environmental pollutants, Australia is a major exporter of it. In fact, 77% of its electricity comes from coal-based power plants, and these create 27% of the country’s total carbon emissions (Commonwealth of Australia 2017). In 2016 alone, Australia produced about 6.9% of world production (503 Mt out of a total of 7,269 Mt). Its exports account for about 32% of the world’s total coal exports (389 Mt out of a total of 1,213 Mt) from at least 405 coal mines, thus making the country the fourth highest producer and biggest net exporter of coal in the world (IEA 2017). Despite severe criticism of its contribution to emissions and climate change, Australia has shown flexibility and leniency toward its coal-based projects; it has agreed to expand Adani’s Carmichael coal mine while 50-plus applications are awaiting approval, which is about six times more than Canada’s projected proposals (IEA 2016).

Australia is also encouraging, rather than backing away from, more pollutant-based industries, and because of its relaxed regulatory climate, current policies are improperly enforced. CEP is likely to deteriorate because corporations tend to overlook environmental concerns and, regardless of the cost of capital, show no interest in improving CEP voluntarily. Furthermore, the preference of firms in these two countries for internal sources to avoid the higher cost of whatever environmental investment they choose, is consistent with the pecking order theory stated by Myers and Majluf (1984), which could also play a role in the nonsignificant effect of the cost of debt.

The results show that since a significant and positive effect is only found for the United Kingdom, capital structure has a limited effect. The result might indicate that higher leverage helps UK firms improve their CEP. This could be possible when the borrowed funds are invested in sustainability projects, or when debt covenants put direct or indirect compliance requirements in place. However, for the other three countries, there is consistent confirmation that capital structure has no significant effect on CEP.

The control variables provide broader confirmation of the positive effects of firm size and age across the countries. Growth and beta appear to have positive effects on CEP only in the United Kingdom, which means the firms that grow faster and take market reactions and movements into account are likely to have a better CEP. Higher growth can be linked to higher CEP when the growth is aligned with environmental considerations. The result on beta remains consistent with the expectation. Furthermore, CAPEX and OCD show positive effects on CEP in the United Kingdom and the United States respectively, which is consistent with the arguments and general expectation cited earlier.

The results suggest that the effects of the variables on CEP are significantly heterogenous at country level because there are wide-ranging differences in environmental and sustainability rules and regulations between countries. These differences may also exist between sectors in a given country, particularly since some sectors in a country may be well regulated, while others are less regulated or not regulated at all. For example, most of the mandatory sector-specific regulations published after 2015 were aimed at the utilities, healthcare, and pharmaceutical sectors (Datamaran 2018). Therefore, it is important to investigate the sector-specific effects of the cost of debt on CEP. As specified in the methodology section, given the sample size limitations, this is applied only to the United States.

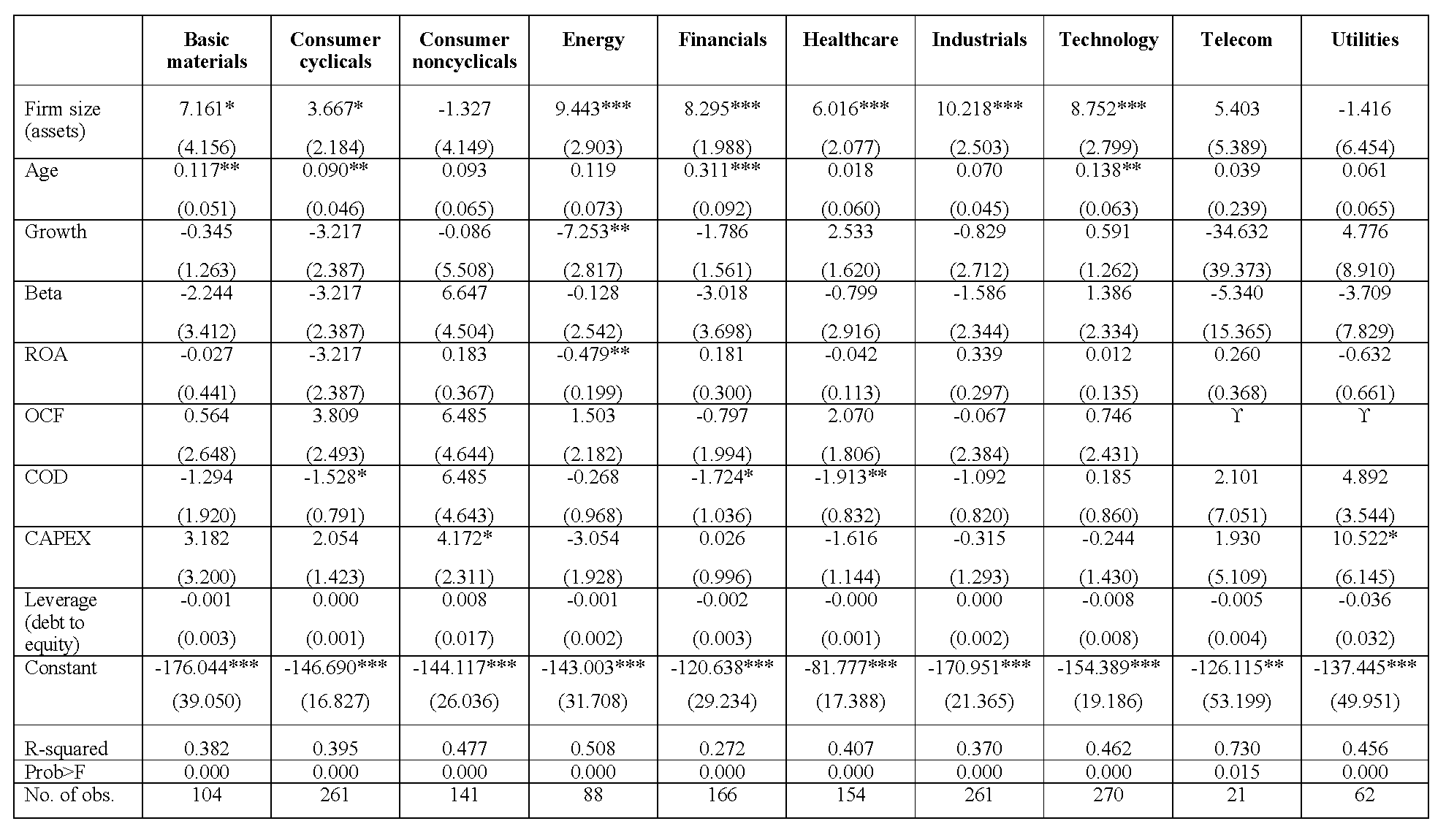

US Industry-Level Investigation

Because of the distribution of the samples across industries, a small number of observations were found for most industries/sectors for the United Kingdom, Australia, and Canada. To maintain the reliability of the estimates, only the sector/industry-wide estimation for the United States is considered because its sample sizes were larger. The sector/industry-wide estimation results for equations (3) and (4), respectively, are presented for the United States (Tables 5 and 6).

CEP has mostly negative sensitivity to the cost of debt for five sectors in particular—consumer cyclical, financials, industrials, healthcare, and telecommunication. However, capital structure (namely degree of leverage) shows no significant effect on CEP in any of the sectors considered.

Consumer cyclical companies show quite different results, for their cost of debt appears to have a negative and significant effect on CEP. Given the higher price of consumer cyclical goods and lumpier cash flows, this sector is defined by a presumed high-price elasticity of demand. As a result, these types of firms may need to prioritize using their cash flows to service debt financing at the expense of CEP. On the other hand, the cost of debt of noncyclical companies shows no significance, perhaps because a presumed low-price elasticity of demand and, therefore, an overall lower cost of debt are characteristic of this sector. However, capital expenditure shows a positive significance to the EP. This could signal that the larger the funds used by a company to acquire, upgrade, and maintain physical assets like property, industrial buildings, or equipment, the higher the EP.

Table 5: USA-Sector-wise Effects of Overall Cost of Debt (equation 3)

= OCF removed to mitigate the significant level of multicollinearity in the initial model. Significance level: ***=1%, **=5%, *=10%.

= OCF removed to mitigate the significant level of multicollinearity in the initial model. Significance level: ***=1%, **=5%, *=10%.Source: Authors’ calculations.

Table 6: USA-Sector-wise Effects of Cost of Long- and Short-Term Debt (equation 4)

= OCF removed to mitigate the significant level of multicollinearity in the initial model. Significance level: ***=1%, **=5%, *=10%.

= OCF removed to mitigate the significant level of multicollinearity in the initial model. Significance level: ***=1%, **=5%, *=10%.Source: Authors’ calculations.

The cost of overall debt has a significant and negative effect on CEP in the financial sector. A similarly significant and negative effect of the cost of long-term debt supports this result. These estimates confirm that a higher cost of debt, particularly long-term debt financing, reduces corporate environmental performance in this sector. The financial sector in the United States is regarded as a highly regulated industry subjected to a higher-than-average degree of competition and stakeholder surveillance, thereby putting constant pressure on profitability and cash flows. A higher cost of debt, particularly long-term debt, could force financial institutions to sacrifice their environmental performance to maintain a certain level of financial strength and stakeholder confidence. In fact, financial institutions seem to be more interested in discussing their role in influencing the environmental performances of borrowing institutions, for example green banking (Rahman and Barua 2016), than they are in their own environmental performance. Their tendency to overlook their own environmental behavior could contribute toward lowering their CEP.

Unsurprisingly, the industrial sector’s cost of long-term debt shows a significant and negative effect on CEP. Damages to the environment caused by industrial processes include, but are not limited to, a decrease in raw materials; a deterioration in the quality of the land, air, and water; the extinction of species; human rights violations; and general environmental pollution. Thus, industrial firms often require important investments to upgrade their current facilities, treat waste, and introduce prevention guidelines and training. Increasing industrial responsibility for “clean” production processes is an important long-term material goal reflected in sensitivity toward the cost of the long-term debt.

The estimates show that a higher overall cost of debt has a significant and negative effect on CEP in the healthcare sector (equation 3). This result is supported by a significant negative effect of the cost of long-term debt (equation 4). Healthcare companies are energy-intensive infrastructures, particularly in the United States, where healthcare businesses are among the most energy-consuming of the sectors. Hospitals are also large waste producers, much of which is clinical waste. Given that consumers are failing to push these types of businesses toward sustainability, environmental initiatives could be very sensitive to the cost of financing. The results show that a higher cost of debt lowers the CEP of firms in this sector.

The cost of short-term debt has a further significant and positive effect on CEP in the telecommunications sector, where most environmental issues stem from the manufacturing process, particularly the disposal of electronic waste. Firms in this sector need to invest heavily to cover the costs of regular inspections and to keep their equipment functioning in line with environmental standards. The higher cost of a short-term debt could help telecom companies improve their CEP. Since this industry is sensitive to litigation lawsuits or other legal actions that may require short-term capital, the solution may perhaps lie in improving the sector’s CEP.

5. Conclusion

All other things being equal, this analysis suggest a main constraint on environmental investment is the cost of debt financing. If environmental investments are to achieve a high environmental performance, corporations must find ways of meeting the heavy initial costs and of ensuring that their investments generate sufficient revenue. When internal equity is not enough to finance such projects, firms use debt and face the risk of incurring higher costs. In fact, many environmental projects have high initial costs and therefore require long-term financing. While the literature includes discussions on accounting approaches to corporate environmental performance, it is evident that comparatively few studies explore how the cost of corporate debt and the structure of capital influence CEP.

This study uses the environmental pillar score from Thomson Reuters ESG data firms drawn from the United States, the United Kingdom, Australia, and Canada to determine the effect of the cost of capital on environmental performance, thus discovering cost of debt to be the main constraint on sustainability investments. Most projects addressing corporate environmental performance have high initial costs and require significant long-term financing. Therefore, the availability and cost of financing are important factors in developing viable new environmental projects. Here, it is recognized that creditors who lend to corporations via loans, bonds, or other types of debt may create an additional impediment to environmental performance, particularly if they charge a high price in the form of interest and fees. A higher cost of financing could limit a firm’s capacity to focus on environmental performance by hampering a manager’s ability to address sustainability issues.

The effect of the cost of debt on CEP could happen in four main ways: (i) firms facing a higher cost of debt financing tend to invest their funds in projects that provide enough financial return to service the cost of debt, rather than in projects that are environmentally responsible or beneficial; (ii) firms raising debt finances at a higher long-term cost could experience significant pressure on their financial performance and financial strength for a long period of time; this prospect could motivate them to undertake projects that are financially attractive but not environmentally responsible; (iii) firms facing a higher cost of debt might need to use CSR-allocated funds in an attempt to service the cost of the debt, particularly during firm-specific crises and systemic downturns in the economy and the financial market; such a diversion of funds could eventually lead a firm to abandon its previously planned CSR or environmentally-related activities for one or several years, and thus reduce the firms’ environmental performance; and (iv) lenders could impose a higher cost on firms that are currently environmentally irresponsible, which could force them to deviate even further from their environmental goals. The likely effects of these four points could be the opposite in cases where firms face a lower cost of debt; in other words, a lower cost of debt would create lower cost burdens, thus allowing firms the flexibility they need to prioritize environmental objectives and thus encourage projects that are both environmentally and financially viable.

From a managerial finance perspective, the association between firms’ cost of debt, degree of leverage, and environmental performance requires a thorough examination. In this article, empirical evidence of this link was provided by using reliable econometric techniques on a large data set of publicly listed corporations in the United States, the United Kingdom, Australia, and Canada. The overall findings indicate that a higher cost of total debt is likely to reduce the environmental performance of companies. In a further examination using separate cost measures we found it is particularly the cost of long-term debt that works as a deterrent. This suggests that long-term projects possibly affect a corporation’s sustainability performance in the long run may be set aside due to a lack of affordable financing.

Biographies

Micol Chiesa is a Lecturer in Circular Economy at Oxford University. Her research focuses on the effect of corporate debt and growth on environmental sustainability across countries. Before landing in Oxford, Micol worked in environmental finance at the Word Bank. She holds a PhD from Oxford University, and an MA from the Johns Hopkins University, School of Advanced International Studies. Micol is a postgraduate fellow at the Royal Geographical Society and a member of the Alliance for Research on Corporate Sustainability.

Suborna Barua is Associate Professor at the Department of International Business, University of Dhaka. He obtained a Doctor of Philosophy (PhD) degree from Federation University Australia and BBA and MBA degrees in Finance from the University of Dhaka, Bangladesh. Dr. Barua holds a 13-year long blended experience of teaching, research, and delivering training and consulting services in the field of finance in national and international settings. He has been teaching courses in finance and banking at universities in both Australia and Bangladesh and delivering a number of professional training courses covering issues in project evaluation and management, financial and investment management, FinTech, financial modelling, and financial markets. Dr. Barua has also worked in several cross-border research projects with the World Bank, the UNDP, the DFID-UK, and the University of Oxford. In addition to teaching and research, Dr. Barua has served in financial and management consultant and advisory roles at more than ten local and multinational financial institutions. He currently heads the Research and Innovation Lab as a consultant at Royal Capital Limited, Dhaka. Dr. Barua has published a book, several book chapters, and over thirty articles in highly ranked and high-impact factor journals. He also currently serves as an editorial board member for several highly ranked finance journals. His research area includes international trade and investment, finance, environment and sustainable development, and machine learning and artificial intelligence applications in finance and economics. A full bio of Dr. Barua and an updated list of his works are available at: Federation University Australia|University of Dhaka| Google Scholar|ResearchGate.

References

Al-Tuwaijri, S. A., T. E. Christensen, and K.E. Hughes II. 2004. “The Relations among Environmental Disclosure, Environmental Performance, and Economic Performance: A Simultaneous Equations Approach.” Accounting, Organizations and Society 29(5–6): 447–71.

Arimura, T. H., A. Hibiki, and H. Katayama. 2008. “Is a Voluntary Approach an Effective Environmental Policy Instrument? A Case for Environmental Management Systems.” Journal of Environmental Economics and Management 55(3): 281–95.

Barua, S., and M. Chiesa. 2019. “Sustainable Financing Practices through Green Bonds: What Affects the Funding Size?” Business Strategy and the Environment 3. https://doi.org/10.1002/bse.2307.

Bauer, R., and D. Hann. 2010. “Corporate Environmental Management and Credit Risk.” ECCE Working Paper, Maastricht University.

Berger, A. N., and E. B. Di Patti. 2006. “Capital Structure and Firm Performance: A New Approach to Testing Agency Theory and an Application to the Banking Industry.” Journal of Banking and Finance 30(4): 1065–102.

Berger, P. G., and E. Ofek. 1995. “Diversification’s Effect on Firm Value.” Journal of Financial Economics 37(1): 39–65.

Berman, S. L., A. C. Wicks, S. Kotha, and T. M. Jones. 1999. “Does Stakeholder Orientation Matter? The Relationship between Stakeholder Management Models and Firm Financial Performance.” Academy of Management Journal 42(5): 488–506.

Borghesi, R., J. F. Houston and A. Naranjo. 2014. “Corporate Socially Responsible Investments: CEO Altruism, Reputation, and Shareholder Interests.” Journal of Corporate Finance 26: 164–81.

Brammer, S., and A. Millington. 2008. “Does It Pay to be Different? An Analysis of the Relationship between Corporate Social and Financial Performance.” Strategic Management Journal 29(12): 1325–43.

Branco, M. C., and L. L. Rodrigues. 2006. “Corporate Social Responsibility and Resource-Based Perspectives.” Journal of Business Ethics 69(2): 111–32.

Buysse, K., and A. Verbeke. 2003. “Proactive Environmental Strategies: A Stakeholder Management Perspective.” Strategic Management Journal 24(5): 453–70.

Chava, S. 2014. “Environmental Externalities and Cost of Capital.” Management Science 60(9): 2223–247.

Chiesa, M., and S. Barua. 2019. “The Surge of Impact Borrowing: The Magnitude and Determinants of Green Bond Supply and Its Heterogeneity across Markets.” Journal of Sustainable Finance and Investment 9(2): 138–61.

Cho, S. Y., C. Lee, and R. J. Pfeiffer Jr. 2013. “Corporate Social Responsibility Performance and Information Asymmetry.” Journal of Accounting and Public Policy 32(1): 71–83.

Cole, M. A., R. J. Elliott, and E. Strobl. 2008. “The Environmental Performance of Firms: The Role of Foreign Ownership, Training, and Experience.” Ecological Economics 65(3): 538–46.

Commonwealth of Australia. 2017. Department of the Environment and Energy Annual Report 2017-2018. Available from: https://www.environment.gov.au/about-us/accountability-reporting/annual-reports [Accessed 20 December 2018].

Cormier, D., and M. Magnan. 1997. “Investors’ Assessment of Implicit Environmental Liabilities: An Empirical Investigation.” Journal of Accounting and Public Policy 16(2): 215–41.

Crifo, P., and V. D. Forget. 2015. “The Economics of Corporate Social Responsibility: A Firm‐Level Perspective Survey.” Journal of Economic Surveys 29(1): 112–30.

Dasgupta, S., H. Hettige, and D. Wheeler. 2000. “What Improves Environmental Compliance? Evidence from Mexican Industry.” Journal of Environmental Economics and Management 39(1): 39–66.

Datamaran. 2018. Datamaran’s Global Insights Report 2018. Available from: https://www.datamaran.com/global-insights-report/ [Accessed 24 November 2018].

Delmas, M. A., and M. W. Toffel. 2008. “Organizational Responses to Environmental Demands: Opening the Black Box.” Strategic Management Journal 29(10): 1027–55.

Derwall, J., K. Koedijk, and J. Ter Horst. 2011. “A Tale of Values-Driven and Profit-Seeking Social Investors.” Journal of Banking and Finance 35(8): 2137–47.

Dhaliwal, D. S., O. Z. Li, A. Tsang, and Y. G. Yang. 2011. “Voluntary Nonfinancial Disclosure and the Cost of equity Capital: The Initiation of Corporate Social Responsibility Reporting.” The Accounting Review 8(1): 59–100.

Dhaliwal, D. S., S. Radhakrishnan, A. Tsang, and Y. G. Yang. 2012. “Nonfinancial Disclosure and Analyst Forecast Accuracy: International Evidence on Corporate Social Responsibility Disclosure.” The Accounting Review 87(3): 723–59.

Dixon-Fowler, H. R., D. J. Slater, J. L. Johnson, A. E. Ellstrand, and A. M. Romi. 2013. “Beyond ‘Does It Pay to Be Green?’ A Meta-Analysis of Moderators of the CEP–CFP Relationship.” Journal of Business Ethics 112(2): 353–66.

Donaldson, T., and L. E. Preston. 1995. “The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications.” Academy of Management Review 20(1): 65–91.

Dragomir, V. D. 2010. “Environmentally Sensitive Disclosures and Financial Performance in a European Setting.” Journal of Accounting and Organizational Change 6(3): 359–88.

Earnhart, D., and L. Lizal. 2007. “Direct and Indirect Effects of Ownership on Firm-Level Environmental Performance.” Eastern European Economics 45(4): 66–87.

Eccles, R. G., G. Serafeim, and M. P. Krzus. 2011. “Market Interest in Nonfinancial Information.” Journal of Applied Corporate Finance 23(4): 113–27.

Economist Intelligence Unit. 2008. Doing Good Business and the Sustainability Challenge. Available from: http://graphics.eiu.com/upload/sustainability_all sponsors.pdf [Accessed 30 October 2018].

El Ghoul, S., O. Guedhami, C. C. Kwok, and D. R. Mishra. 2011. “Does Corporate Social Responsibility Affect the Cost of Capital?” Journal of Banking and Finance 35(9): 2388–406.

Endrikat, J., E. Guenther, and H. Hoppe. 2014. “Making Sense of Conflicting Empirical Findings: A Meta-Analytic Review of the Relationship between Corporate Environmental and Financial Performance.” European Management Journal 32(5): 735–51.

Etzion, D. 2007. “Research on Organizations and the Natural Environment, 1992–Present: A Review.” Journal of Management 33(4): 637–64.

Freeman, R. E. 2010. Strategic Management: A Stakeholder Approach. Cambridge: Cambridge University Press.

Gangadharan, L. 2006. “Environmental Compliance by Firms in the Manufacturing Sector in Mexico.” Ecological Economics 59(4): 477–86.

Gebhardt, W. R., C. M. Lee, and B. Swaminathan. 2001. “Toward an Implied Cost of Capital.” Journal of Accounting Research 39(1): 135–76.

Gode, D., and P. Mohanram. 2003. “Inferring the Cost of Capital Using the Ohlson–Juettner Model.” Review of Accounting Studies 8(4): 399–431.

Goss, A., and G. S. Roberts. 2011. “The Impact of Corporate Social Responsibility on the Cost of Bank Loans.” Journal of Banking and Finance 35(7): 1794–810.

Harris, M., and A. Raviv. 1991. “The Theory of Capital Structure.” Journal of Finance 46(1): 297–355.

Harrison, J. S., and A. C. Wicks. 2013. “Stakeholder Theory, Value, and Firm Performance.” Business Ethics Quarterly 23(1): 97–124.

Hart, S. L. 1995. “A Natural-Resource-Based View of the Firm.” Academy of Management Review 20(4): 986–1014.

Henri, J. F., and M. Journeault. 2010. “Eco-Control: The Influence of Management Control Systems on Environmental and Economic Performance.” Accounting, Organizations and Society 35(1): 63–80.

Herremans, I. M., P. Akathaporn, and M. McInnes. 1993. “An Investigation of Corporate Social Responsibility Reputation and Economic Performance.” Accounting, Organizations and Society 18(7–8): 587–604.

Hillman, A. J., and G. D. Keim. 2001. “Shareholder Value, Stakeholder Management, and Social Issues: What’s the Bottom Line?” Strategic Management Journal 22(2): 125–39.

Hong, H., and M. Kacperczyk. 2009. “The Price of Sin: The Effects of Social Norms on Markets.” Journal of Financial Economics 93(1): 15–36.

IEA (International Energy Agency). 2016. Medium-Term Coal Market Report. Available from: https://www.iea.org/reports/medium-term-coal-market-report-2016 [Accessed 18 November 2018].

IEA (International Energy Agency). 2017. Key World Energy Statistics. Available from: https://www.iea.org/publications/freepublications/publication/KeyWorld (2017). pdf [Accessed 18 November 2018]. Also available from http://svenskvindenergi.org/wp-content/uploads/2017/12/KeyWorld2017.pdf

Ioannou, I., and G. Serafeim. 2015. “The Impact of Corporate Social Responsibility on Investment Recommendations: Analysts’ Perceptions and Shifting Institutional Logics.” Strategic Management Journal 36(7): 1053–81.

Jensen, M. C. 1986. “Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers.” The American Economic Review 76(2): 323–9.

Jensen, M. C., and W. H. Meckling. 1976. “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure.” Journal of Financial Economics 3(4): 305–60.

Jiang, L., C. Lin, and P. Lin. 2014. “The Determinants of Pollution Levels: Firm-Level Evidence from Chinese Manufacturing.” Journal of Comparative Economics 42(1): 118–42.

Jones, T. M. 1995. “Instrumental Stakeholder Theory: A Synthesis of Ethics and Economics.” Academy of Management Review 20(2): 404–37.

Kassinis, G., and N. Vafeas. 2006. “Stakeholder Pressures and Environmental Performance.” Academy of Management Journal 49(1): 145–59.

Khanna, M., and L. A. Damon. 1999. “EPA’s Voluntary 33/50 Program: Impact on Toxic Releases and Economic Performance of Firms.” Journal of Environmental Economics and Management 37(1): 1–25.

King, A. A., M. J. Lenox, and A. Terlaak. 2005. “The Strategic Use of decentralized Institutions: Exploring Certification with the ISO 14001 Management Standard.” Academy of Management Journal 48(6): 1091–1106.

Lambert, S. C., A. J. Carter, and R. L. Burritt. 2012. Recognising Commitment to Sustainability through the Business Model. Centre for Accounting, Governance and Sustainability, University of South Australia.

Lang, M., and R. Lundholm. 1993. “Cross-Sectional Determinants of Analyst Ratings of Corporate Disclosures.” Journal of Accounting Research 31(2): 246–71.

Lefebvre, É., L. A. Lefebvre, and S. Talbot. 2003. “Determinants and Impacts of Environmental Performance in SMEs.” RandD Management 33(3): 263–83.

Luo, X., H. Wang, S. Raithel, and Q. Zheng. 2015. “Corporate Social Performance, Analyst Stock Recommendations, and Firm Future Returns.” Strategic Management Journal 36(1): 123–36.

Mackey, A., T. B. Mackey, and J. B. Barney. 2007. “Corporate Social Responsibility and Firm Performance: Investor Preferences and Corporate Strategies.” Academy of Management Review 32(3): 817–35.

McWilliams, A., and D. Siegel. 2001. “Corporate Social Responsibility: A Theory of the Firm Perspective.” Academy of Management Review 26(1): 117–27.

Majumdar, S. K., and P. Chhibber. 1999. “Capital Structure and Performance: Evidence from a Transition Economy on an Aspect of Corporate Governance.” Public Choice 98(3–4): 287–305.

Margolis, J. D., and J. P. Walsh. 2003. “Misery Loves Companies: Rethinking Social Initiatives by Business.” Administrative Science Quarterly 48(2): 268–305.

Magnanelli, B. S., and M. F. Izzo. 2017. “Corporate Social Performance and Cost of Debt: The Relationship.” Social Responsibility Journal 13(2): 250–65.

Martínez, F. J., and A. J. V. Frías. 2015. “Relationship between Sustainable Development and Financial Performance: International Empirical Research.” Business Strategy and the Environment 24(1): 20–39.

Miles, S. 2017. “Stakeholder Theory Classification: A Theoretical and Empirical Evaluation of Definitions.” Journal of Business Ethics 142(3): 437–59.

Mitchell, R. K., B. R. Agle, and D. J. Wood. 1997. “Toward a Theory of Stakeholder Identification and Salience: Defining the Principle of Who and What Really Counts.” Academy of Management Review 22(4): 853–86.

Myers, S. C., and N. S. Majluf. 1984. “Corporate Financing and Investment Decisions When Firms Have Information That Investors Do Not Have.” Journal of Financial Economics 13(2): 187–221.

Ng, A. C., and Z. Rezaee. 2015. “Business Sustainability Performance and Cost of Equity Capital.” Journal of Corporate Finance 34(C): 128–49.

O’Brien, R. M. 2007. “A Caution Regarding Rules of Thumb for Variance Inflation Factors.” Quality & Quantity 41(5): 673–90.

Oikonomou, I., C. Brooks, and S. Pavelin. 2014. “The Effects of Corporate Social Performance on the Cost of corporate Debt and Credit Ratings.” Financial Review 49(1): 49–75.

Orlitzky, M., F. L. Schmidt, and S. L. Rynes. 2003. “Corporate Social and Financial Performance: A Meta-Analysis.” Organization Studies 24(3): 403–41.

Palley, T. I. 2013. “Financialization: What It Is and Why It Matters.” In Financialization: The Economics of Finance Capital Domination, by T. I. Palley.London: Palgrave Macmillan: 17–40.

Patten, D. M. 2002. “Media Exposure, Public Policy Pressure, and Environmental Disclosure: An Examination of the Impact of TRI Data Availability.” Accounting Form 26(2): 152–71.

Porter, M. E., and M. R. Kramer. 2006. “The Link between Competitive Advantage and Corporate Social Responsibility.” Harvard Business Review 84(12): 78–92.

Porter, M. E., and C. Van der Linde. 1995. “Toward a New Conception of the Environment-Competitiveness Relationship.” Journal of Economic Perspectives 9(4): 97–118.

Poser, C., E. Guenther, and M. Orlitzky. 2012. “Shades of Green: Using Computer-Aided Qualitative Data Analysis to Explore Different Aspects of Corporate Environmental Performance.” Journal of Management Control 22(4): 413–50.

Qi, G. Y., S. X. Zeng, J. J. Shi, X. H. Meng, H. Lin, and Q. X. Yang. 2014. “Revisiting the Relationship between Environmental and Financial Performance in Chinese Industry.” Journal of Environmental Management 145: 349–56.

Rahman, S. M., and S. Barua. 2016. “The Design and Adoption of Green Banking Framework for Environment Protection: Lessons from Bangladesh.” Australian Journal of Sustainable Business and Society 2(1): 1–19.

Russo, M. V., and P. A. Fouts. 1997. “A Resource-Based Perspective on Corporate Environmental Performance and Profitability.” Academy of Management Journal 40(3): 534–59.