Defining Climate-Aligned Investment: An Analysis of Sustainable Finance Taxonomy Development

1,471

The global transition toward a low-carbon and climate-resilient economy requires common, science-based frameworks against which governments, the private sector, and individuals can determine whether activities…

Katie House, MSc

Senior Research Analyst, Climate Bonds Initiative

Lionel Mok, MSc

Researcher, Hong Kong University of Science and Technology; Research Analyst, Climate Bonds Initiative

Aneil Tripathy, MA

Researcher, Brandeis University

Abstract

The green bond market has grown rapidly since its inception in 2007. Climate-aligned standards provide investors with the confidence that their investments deliver a measurable climate benefit. Serving as a benchmark, these standards demonstrate alignment with the Paris Agreement, against which green bond issuers can then report compliance. This paper draws on the authors’ experiences as practitioners and researchers helping to develop the Climate Bonds Standard and the European Union’s Sustainable Finance Taxonomy to analyze the methodological considerations that were vital to the development of both taxonomy systems. The first section positions the role of standards development within the context of the green bond market and is followed by an analysis of the factors that affect the Climate Bonds Standard criteria development process. This paper concludes with key takeaways and suggestions for areas of future research on climate-aligned standards development.

1. Introduction: Defining Climate-Aligned Investment: An Analysis of Sustainable Finance Taxonomy Development

The global transition toward a low-carbon and climate-resilient economy requires common, science-based frameworks against which governments, the private sector, and individuals can determine whether activities contribute meaningfully to that transition. Developing a standardized language for determining what activities contribute to climate change mitigation and adaptation is a primary focus of international policymaking efforts to meet the Paris Agreement targets.

In March 2020, the EU Technical Expert Group (TEG) on Sustainable Finance released its final recommendations to the European Commission (the Commission) on the EU Taxonomy, outlining the technical screening criteria that determine whether an economic activity is environmentally sustainable. An increasing number of countries and jurisdictions are developing parallel climate-aligned investment guidelines that will help to determine the climate impacts of financial portfolios. Developing a better understanding of methodological considerations inherent within the taxonomy design process will enable policymakers to implement and improve on the sustainable finance taxonomy work that has been done at the EC level and previously by the Climate Bonds Initiative (Climate Bonds). Climate Bonds is a nongovernmental organization that has been developing the concept of a climate-aligned taxonomy through their Climate Bond Initiative Taxonomy (CBI Taxonomy) for over a decade (Kidney et al. 2009).

Although the EU Taxonomy and the CBI Taxonomy both focus on outlining what is eligible for sustainable and climate-aligned finance, the standards have been developed by organizations that are dramatically different in terms of size, capacity, and convening power. While these contextual factors may limit the comparability of the processes, the intention of this paper is simply to open the dialogue on what constitutes a good “standard-setting” process in the context of institutional realities and constraints.

In this paper, we start with a historical reflection on the development of sustainable finance standards before comparing taxonomy developments at both Climate Bonds and the Commission. We compare the overall processes of the two taxonomies before directly comparing how the expert groups were formed, the discussions were managed, and the decisions were made, as well as how public consultations, board approvals, and reviews occurred. By drawing on the first-hand and lived experiences of the authors, this paper highlights the different group and knowledge production dynamics that can arise from taxonomy development. We conclude with some key takeaways from both the CBI Taxonomy and the EU Taxonomy experiences in order to propose a set of guidelines for future taxonomy development.

2. Background

The bulk of climate-finance research, particularly within the green bond space, centers on the concept of pricing advantages available to green bond issuers (Kapraun and Scheins 2019; Bachelet, Becchetti, and Manfredonia 2019; Hachenberg and Schiereck 2018; Karpf and Mandel 2018; Larcker and Watts 2020; Partridge and Medda 2020; Zerbib 2019; Wulandari et al. 2018). A growing body of research is emerging on the role of policy frameworks in mobilizing climate finance (Edwards 2004; Lovell 2013; Lovell 2015). However, further investigation is needed into the methodological considerations that may affect the rules of a taxonomy if the field is to gain more credence within academic literature.

Social scientists have analyzed processes of standardization in markets through detailing the construction of devices (Lovell 2013; Mackenzie 2008; Riles 2011). These studies outline a method of study for standardization through tracing both the production of standards themselves as well as the organizational relationships. The proliferation of environmental standards is reinvigorating these academic discussions on the leveraging

of scientific knowledge for markets and policymaking. As Paul Edwards notes in his reflection on standards as social technology, “[d]etecting climate change depends on global standards. . . . Stable scientific knowledge depends on the successful negotiation of such standards” (Edwards 2004, 827). As a method for transforming science into policy, the sustainable finance taxonomy process is in a unique position to build a bridge between policymakers and scientists in a way that has not been done before, through highlighting environmental and climate concerns (Linnenluecke, Smith, and McKnight 2016). This negotiation from science to industry standards allows investors, policymakers, and the public at large to comprehend the environmental and climate impacts of their decisions. Climate standards demonstrate the “the irreducible social and political dimensions of all technological systems,” (Edwards 2004, 828). Climate standards in climate finance bring to the forefront questions of what a market is, how policymakers and government interact with finance, and what ultimately is the role of finance in society (Tripathy 2017; Silver 2017).

3. Emergence of Standards for Sustainable Finance

In the early years of the green bond market, the general consensus among market participants was that standards or any type of regulation on what projects were eligible to be included in green bond financing would stifle market growth and that scrutiny from investors or second party opinion providers was enough to maintain the integrity of the green bond market (Wood and Grace 2011).

When the European Investment Bank (EIB) and the World Bank issued the world’s first green bonds, these institutions developed frameworks for disclosing details on projects, but they did not overtly define what eligible use of proceeds should be for green bonds. In their first green bond issuances, the EIB and World Bank each created frameworks. These two frameworks provided templates that could be used by future green bond issuers. They also helped policymakers align infrastructure portfolios with Paris Agreement targets. In a green bond market reflection from the EIB, the bank argues that “[p]olicy making is about clear indication of public priorities within those [market] alternatives” (European Investment Bank 2017). It was around 2013, with the experience of steady growth in the green bond market, that a philosophical rift widened among market participants. There were those who argued that a system of principles was necessary to guide the market. This was demonstrated by the development of the Green Bond Principles (GBPs), convened by the International Capital Markets Association (ICMA). As the market continued to grow at pace in 2013, the GBPs were established by a consortium of investment bank bond underwriters to provide conformity among green bond issuance (Bowman 2015, 208). At that time, and since, the GBPs have only included broad Use of Proceeds (UoP) categories for defining what is green (Kidney 2013). This approach was in contrast with the proponents of standardization who emphasized the importance of a common framework for transforming science into a sustainable finance taxonomy.

One market organization, the nonprofit Climate Bonds Initiative, ignored dismissals of standards and worked from its inception to establish a sustainable taxonomy to evaluate infrastructure financed by green bonds in relation to climate emissions scenarios (Kidney 2009). In 2012, the first CBI Taxonomy was published, with criteria for solar and wind being its initial foci (Pell 2013). Sean Kidney, co-founder and CEO of Climate Bonds, worked to establish the CBI Taxonomy to ensure that the green bond market was mobilized effectively to finance projects and assets that delivered climate change solutions. According to Kidney:

The idea initially was that if we change the planet quickly, we have to be clear on what we are going to do. We need a common global approach. . . . If we want investors to drive change, we need to have consensus. We need a strong enabling state to make the change, but we also need to make sure the changes are science driven. So, the whole idea of the standards was to create a science driven artefact to push change.

Through its consultations with academics focused on standards development, Climate Bonds began the process of creating a robust standard based on climate science in order to evaluate the UoP underpinning green bonds (McDermott, Noah, and Cashore 2008). While it’s important to clarify the distinction between principles and standards—principles providing a framing of what is green, and standards establishing substantive criteria for evaluating green claims—in practice the two concepts work hand in hand. The Climate Bonds Standard is made up of two parts: the overarching standard that applies to green bonds financing projects in any sector and sector criteria that have specific thresholds. These criteria are the technical requirements of the CBI Taxonomy. Together, the GBPs and the Climate Bonds Standard and CBI Taxonomy have become the cornerstones of green bond market policy frameworks today, encouraging other jurisdictions to develop similar guidance.

In 2015, the People’s Bank of China (PBoC) and the National Development and Reform Commission (NDRC) each published their own guidelines for issuing green bonds in China. The CBI Taxonomy was used to develop these green bond market frameworks (Nan and Wang 2016). Similarly, in supporting efforts to protect the environment, the ASEAN Capital Markets Forum (ACMF) launched the ASEAN Green Bond Standards (ASEAN GBS)—based on the GBPs—to help in the allocation of resources toward climate-friendly investments in the region. Since its launch in November 2017, the ASEAN GBS has gained encouraging traction in the region, with three successful green bonds from Malaysia and Singapore carrying the ASEAN GBS label (ACMF 2017)

The latest move by the Commission to develop the EU Taxonomy, the PBoC’s rule book, and the increasing usage of the CBI Taxonomy by green bond issuers, highlights the growing popularity of using a taxonomy to define what constitutes a low-carbon, climate-resilient economy. Although it would be ideal to compare the taxonomy development processes in China with those of the Commission and Climate Bonds, the authors can only access secondary and piecemeal information about the process in China. Further investigation in this area would be a welcome development. Thus, here we focus on our experiences with the Climate Bonds Standard and the EU Taxonomy.

4. Overall Processes of CBI Taxonomy and EU Taxonomy

The processes underpinning the development of the CBI Taxonomy and the EU Taxonomy produce the frames through which both taxonomies interpret climate science for financial markets. The comparison here is particularly pertinent because the Commission process is based, in part, on Climate Bonds’ experience (Financial Stability, Financial Services and Capital Markets Union 2019). Similarly, future taxonomy development work is likely to draw on both of these criteria. The International Organization for Standardization (ISO) is currently developing its own climate-aligned taxonomy, which is also expected to draw on both the Commission’s and Climate Bonds’ experiences (Gould 2018). The processes used are interesting to study both separately and comparatively because they are similar but have some significant structural and organizational differences, which may have affected the outcomes. Here we present both the CBI Taxonomy and EU Taxonomy processes separately and comparatively.

5. CBI Taxonomy: Criteria Development Process

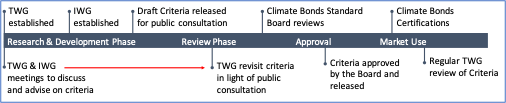

Sector-specific criteria can be combined to create a taxonomy for sustainable finance. Since its inception in 2011, the CBI taxonomy has expanded in scope and published criteria for an increasing variety of sectors. The process for developing the standard and sector criteria begins with the establishment of the working groups and includes several phases (Figure 1).

Figure 1: The Process for Developing the CBI Taxonomy Overarching Standard and Sector Criteria

Source: Climate Bonds, 2018.

In the CBI Taxonomy process, discussions cover guiding principles for criteria, the scope of the criteria, and the metrics and thresholds for determining whether an investment is climate-aligned. Technical Working Groups (TWGs) and Industry Working Groups (IWGs) hold separate discussions on a bimonthly basis; these discussions are led by a technical consultant who is hired by Climate Bonds to lead the criteria development process based on their expertise. A TWG is composed of academic and technical experts in the specific area that criteria are being developed; they often work for universities, NGOs, consultancies, or intergovernmental agencies. An IWG is composed of potential green bond issuers, investors, verifiers, and other companies and entities involved in the infrastructure category.

Once the TWG and IWG have concluded their discussions and finalized draft criteria, those criteria are released for public consultation. The Climate Bonds Standards Board then gives the final approval for criteria to be used for Climate Bonds Certification. According to its design, this process is multi-stakeholder, grounded in the latest environmental and climate science, draws on expert input, and provides space for existing initiatives to be leveraged wherever appropriate to do so.

6. EU Taxonomy: Criteria Development Process

In response to growing interest and the development of numerous types of sustainable finance, the Commission launched a High-Level Expert Group (HLEG) on sustainable finance to provide recommendations for a comprehensive EU strategy on the subject as part of the Capital Markets Union (European Commission 2016). In January 2018, the HLEG published its final report, which contained eight key recommendations, other cross-cutting recommendations for financial institutions, sectoral recommendations, social recommendations, and broader environmental sustainability recommendations. The establishment and the maintenance of a common sustainable finance taxonomy at the EU level were the first two of the key recommendations made by the HLEG (Financial Stability, Financial Services and Capital Markets Union 2018a). In the May 2018 follow-up, the Commission established the EU TEG on Sustainable Finance, which was mandated to develop a sustainable finance taxonomy in its general assessment of sustainable finance (European Commission 2020a).

The HLEG essentially provided the mandate the Commission needed before it could prioritize developing a sustainable finance taxonomy. The Commission has a high level of convening power but must have a strong mandate before it can embark on a project as large as one establishing a sustainable finance taxonomy. The preliminary work and recommendations from the HLEG gave the TEG’s work validity and momentum, which helped the TEG process to meet the tight timescales designated by the Commission.

The TEG took a divide and conquer approach to developing the taxonomy. TEG members were appointed to chair the development of criteria for economic sectors (energy, waste management, forestry, agriculture, transport, manufacturing, and adaptation and resilience). The chairs were supported by other TEG members and external experts who were screened and included through an additional EU Taxonomy (European Commission 2019). Similarly, Climate Bonds appoints a lead analyst from within the organization and hires a technical consultant to manage the development of each sector criteria.

EU Taxonomy discussions were organized according to a template that scoped sustainability issues, developed principles, and identified relevant legislation. The template also proposed indicators, thresholds, and trajectories for infrastructure sectors. These were provided as summary tables in the TEG’s Technical Report. To design this development process, the TEG looked at what had been done before in sustainable finance to assess climate alignment, such as the CBI Taxonomy and the EIB’s framework. The group also recognized the need for taxonomy development to be multi-stakeholder and grounded in the latest environmental and climate science.

The most striking difference between the EU and CBI taxonomies is the scale of the Commission’s project and the simultaneous development of multiple criteria on a tight timeframe. In the CBI Taxonomy, criteria are developed independently of one another. Newer criteria development work builds on the principles and practices that emerge in older CBI Taxonomy criteria. In this sense, the CBI Taxonomy development has been more iterative than the EU Taxonomy.

From this outline of the criteria development process for both the Climate Bonds Standard and the EU Taxonomy, we now move to compare parts of these processes to recognize similarities, differences, and aspects that worked well, and to propose recommendations for future improvements. Here we discuss the formation of expert groups, management of discussions, decision-making structures, and the consultation phase for the TEG’s and Climate Bonds’ taxonomy developments.

7. Multi-Stakeholder Input

The credibility of a standard development process rests on the availability of technical and industry knowledge, and the ability to feed this information systematically into final agreements on sector criteria. Ensuring that there is a robust and sufficient representation of expertise from the relevant stakeholders can be accomplished through the formation of expert groups, but also during the public consultation when the criteria are circulated among a wider audience for feedback. This section outlines the key considerations taken by Climate Bonds and the Commission when forming expert groups and conducting public consultation.

How Are Climate Bonds’ TWGs and IWGs Formed?

CBI Taxonomy criteria development draws on the organization’s professional and industry networks to form TWGs and IWGs. Depending on the sector, Climate Bonds may also approach individuals or organizations that it has not previously had any connection with to see if they will participate in either a TWG or an IWG. Often receptive, these organizations or individuals see participation as an opportunity to apply sector-specific climate-change knowledge to a financial context and see the benefit of creating criteria for financial markets.

How Were the TEG Sector Working Groups Formed?

The Commission received 185 applications from 62 individuals and 123 organizations in response to its call for TEG membership applications (Financial Stability, Financial Services and Capital Markets Union 2018b). Some organizations proposed several individuals, leading to roughly 240 people who needed to be reviewed. A team of 15 reviewers from the EU’s Directorate Generals (DGs), including the DG for Climate Action, DG for Environment, and DG for Financial Stability, Financial Services and Capital Markets Union, reviewed all applications. A minimum of two reviewers evaluated each applicant. The most important selection criteria in the review process were: (1) proven knowledge and expertise for one of the subtasks and (2) knowledge on the intersection between finance and the environment.

The Commission also considered the need for a balanced representation of relevant expertise and areas of interest, geographical distribution, gender distribution, and a sufficiently wide variety in the representation of financial and real economic actors and sectors. The selection process resulted in a group of individuals with 17 nationalities. Among the members, 15 out of 35 were women (European Commission 2018). Once sectors were assigned to the different co-chairs, a second call for external experts was made. These applicants were then screened by the TEG members co-chairing the respective sectors.

In both the TEG and Climate Bonds’ TWGs and IWGs, expert groups are composed of a diverse and balanced representation of stakeholders. To form the TWGs and IWGs, Climate Bonds relied on professional networks and working relationships with the experts. These networks have grown over time as the organization has established itself in the green bond market and in climate finance at large. However, despite its strong position in the market, Climate Bonds does not have the convening power of the Commission as a political organization. In this sense, the Commission was able to encourage high-level stakeholder engagement and also leverage the expertise and resources available through the respective Directorate Generals. The efficiency with which the TEG criteria were developed was due to the convening power of the Commission. Similarly, the ability of the Commission to host TEG meetings and workshops throughout the consultation period helped facilitate a higher level of engagement and knowledge sharing.

This convening power is important to taxonomy development because the criteria attempt to convert scientific knowledge into industry-applicable rule sets that strike a balance between scientific rigor, ambition, and usability. The higher the convening power, the more likely it is that three things will be achieved: first, the right people for the criteria development will be recruited; second, enough experts will be recruited, both in terms of absolute numbers and diversity of experience, location, and gender; and finally, the members of the expert group will be committed to the objective and motivated to give time to achieving it.

Throughout the CBI and EU taxonomy development processes, the composition of expert groups is critical to the group’s final output and the credibility of the criteria established. Organizations, such as the UK-based nonprofit InfluenceMap, track the presence and effect of lobbying and interest groups on the policy formation process. Its reports highlight the need to ensure that such expert groups are isolated from industry influences, which may be counterintuitive to the climate-agenda (InfluenceMap 2019). For the CBI Taxonomy, the availability of professional networks ensured that the TWGs and IWGs were populated by experts who would not compromise the organization’s objectives. Similarly, the Commission’s convening power was vital to ensuring that appropriate filtering could produce enough applicants with an adequate level of expertise and avoid industry influence.

8. Discussion Management

Discussions between Climate Bonds Standard’s TWGs and IWGs are led by consultants through webinars and supported by presentations, a draft issues paper that develops into a final summary of the criteria, and a separate background document that provides details of the discussions. The issues paper outlines the role of decarbonization within and of the sector. The TWG and IWG then discuss principles, metrics, and thresholds over the consultation period. Climate Bonds has found it most productive to put in front of the TWG and IWG the proposals for criteria and thresholds, which can then be questioned and amended. Open discussions can cause scope creep and can make the process a bit overwhelming for the TWG and IWG in knowing where to start. It is always stressed that proposals are just that, and they can be fully rejected or completely reworked.

In the EU Taxonomy process, a predesigned template provided for all sectors guided the co-chairs. The template was completed over the course of the discussions and covered the climate impact of the sector, sector-specific principles for criteria design, proposed metrics, thresholds, and economic and social impacts. These templates accelerated discussions and kept TEG outcomes comparable across sectors.

One distinguishing feature between two taxonomy development processes was the use of the Statistical Office of the European Communities’ NACE (Nomenclature des Activités Économiques dans la Communauté Européenne) codes to define the economic activities to which criteria would be developed. This helped to limit the scope of the TEG’s work and was an important evolution from the process used by Climate Bonds, which prioritized sector criteria development based on climate change mitigation potential and demand from the green bond market.

One noticeable strength of the EC TEG process was that in addition to the webinars and teleconferences, the EU was able to facilitate in-person meetings between the TEG members and external experts in Brussels. While we cannot quantify the value of these meetings, it was clear that these interactions were vital for breaking communication barriers and building trust between individuals. From our lived experiences, it seems that consensus forming was more efficient when stakeholders were physically gathered together. As an NGO, Climate Bonds does not have the capacity to arrange and facilitate these in-person interactions, which has made it more difficult and time-consuming to reach a consensus between members.

9. Public Consultation

A public consultation helps ensure both the credibility and usability of taxonomies. The development of the CBI Taxonomy and the EU Taxonomy showed the importance of conducting a public consultation that allows stakeholders who were not directly involved in the process to feed into the final criteria. In both cases, efforts were made to ensure that the maximum number of people were aware that the criteria were being made available for public feedback (European Commission, 2020b).

10. Decision Making

Decision-making power at Climate Bonds rests with the TWG, and unanimity is required among TWG members. Consulted for its expertise, the TWG functions primarily to ensure that the criteria are scientifically and technically robust. The IWG is relied on to provide an industry perspective on the usability and feasibility of the criteria. The IWG does not have decision-making authority over the criteria, and consensus among the IWG members is not a requirement. This is because it is recognized that while the IWG has an important perspective to capture, in some cases, members may also have an incentive to weaken the criteria—for example, if they are a potential future issuer that may use the criteria for Climate Bond Certification. But the technical lead and researcher work to ensure that all considerations and perspectives are represented in the criteria.

Both Climate Bonds and the TEG sought to achieve consensus on the criteria from within the groups. Neither formally asked group members to vote for their approval of the final criteria, but chairs sought to address any objections and concerns raised by group members. Reaching consensus within the groups was found to be important because each group member represents a perspective from within the market and should not be viewed as an outlier opinion.

11. Conclusion

Over the last ten years, taxonomy development has expanded to different countries and to cover various activities and assets and projects. During this period, the process for producing criteria has evolved from both institutional learnings and trial-and-error. The EU Taxonomy managed to produce specific criteria for 67 economic activities across 8 economic sectors in under 18 months.

One of the factors that enabled the TEG to produce these criteria so efficiently was the use of the standardized template that focused the technical discussions on scoping the activity, setting sustainability objectives, and identifying suitable metrics. We recommend using a similar structure and template for future taxonomy-related discussions. Another important facet of the EC TEG approach was to use the EU NACE codes for guidance in selecting the economic sectors to develop criteria. This provided a systematic means to ensure that the most pertinent activities within a sector were addressed. Expert groups must represent a wide range of expertise from various industries, geographies, and types of institutions. In the absence of a widely recognized body that can utilize its convening power, an organization needs to leverage its existing networks while being mindful of the bias this may bring to the expert group.

The cohesion and success of these discussions depends on how well the group is able to align on the objectives of the taxonomy. The EU Taxonomy experiences highlight the importance of in-person meetings to facilitate dialogue and, when these are not possible, how online conferencing is crucial to maintaining discussions. Similarly, ensuring that stakeholders who are not directly involved in the process have the ability to feed in through public consultation processes is critical. Finally, establishing a process for decision making within the various steps of a taxonomy development process is also vital.

12. Research Summary

In this paper, we have identified steps within the climate-aligned taxonomy development process that policymakers and those tasked with developing future taxonomies will have to take. Expert groups should represent a wide range of interests and bodies of knowledge, and these different voices should be managed by an appointed head in order to keep discussions pointed to drafting coherent criteria. We hope that these comparisons between the CBI Taxonomy and the EU Taxonomy processes can provide insight and a structured approach for how to construct sustainable taxonomies that are functional for multiple stakeholder groups. From our experience, the robustness, credibility, and usability of the CBI Taxonomy and EU Taxonomy processes are heavily dependent on the composition of the groups and the quality of their discussions.

Biographies

Katie House holds an MSc in Environmental Technology from Imperial College London and a BSc in Geographical Sciences from the University of Bristol. She previously worked at Climate Bonds Initiative on the development of the Climate Bonds Standard and contributed to Climate Bonds’ work on the EU Sustainable Finance Taxonomy. Katie is now an analyst at Affirmative Investment Management, a dedicated fixed income impact investor.

Lionel Mok has an MSc in the Economics and Policy of Energy and the Environment from University College London. He has worked as a journalist in Cambodia and Dubai, and was a consultant for the International Finance Corporation from 2016 to 2018. He currently works as Policy Manager for the Climate Bonds Initiative in London and is a PhD Candidate at the Hong Kong University of Science and Technology.

Aneil Tripathy is a PhD Candidate in economic anthropology at Brandeis University, where his research focuses on the growth of climate finance and the green bond market. Aneil has been a visiting researcher at Cass Business School, University College London, and the Pentland Centre at Lancaster University. He has worked in climate finance for five years as a researcher, executive associate, and academic research consultant at the Climate Bonds Initiative, and as a consultant for the Clean Energy States Alliance. Aneil has training in environmental economics, ethnographic research, and systems thinking.

References

ASEAN Capital Markets Forum (ACMF). 2017. “ASEAN Green Bond Standards.” Available from https://www.theacmf.org/images/downloads/pdf/AGBS2018.pdf.

Bachelet, Maria Jua, Leonardo Becchetti, and Stefano Manfredonia. 2019. “The Green Bonds Premium Puzzle: The Role of Issuer Characteristics and Third-Party Verification.” Sustainability 11:1098.

Bowman, Megan. 2015. Banking on Climate Change: How Finance Actors and Transnational Regulatory Regimes Are Responding. Kluwer Law International.

Climate Bonds Initiative (CBI) and China Central Depository & Clearing Company. 2018. China Green Bond Market 2017. Available from https://www.climatebonds.net /files/reports/china_annual_report_2017_en_final_14_02_2018.pdf.

Climate Bonds Initiative. 2018. CBI Forestry Criteria. Available from https://www.climatebonds.net/files/files/CBI_Background%20Doc_Forests_November%202018%282%29.pdf.

Cooper, S., P. Stokes, Y. Liu, and S. Tarba. 2017. “Sustainability and Organizational Behavior: A Micro‐Foundational Perspective.” Journal of Organizational Behavior 38(9): 1297–1301.

Edwards, Paul N. 2004. “A Vast Machine: Standards as Social Technology.” Science 304:827–828.

European Commission. 2016. “European Commission appoints members of the High-Level Expert Group on sustainable finance.” European Commission. Available from https://europa.eu/rapid/press-release_IP-16-4502_en.htm?locale=en.

European Commission. 2018. “Frequently Asked Questions.” Technical Expert Group (TEG) on Sustainable Finance. Available from https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/sustainable-finance-teg-frequently-asked-questions_en.pdf.

European Commission. 2019. “List of selected experts that will be invited to the workshops on sustainable finance taxonomy.” Available from https://ec.europa.eu/info/files/sustainable-finance-taxonomy-workshops-list-invited-experts_en.

European Commission. 2020a. “EU Taxonomy for Sustainable Activities.” Available from https://ec.europa.eu/info/publications/sustainable-finance-teg-taxonomy_en#200903.

European Commission. 2020b. “Technical Expert Group on Sustainable Finance.” Available from https://ec.europa.eu/info/publications/sustainable-finance-technical-expert-group_en.

European Investment Bank. 2017. “10 Years of Green Bond Issuance at EIB: Developing a Lingua Franca for Green Bonds.” Global Capital. Available from https://www.globalcapital.com/article/b144nc1gwdpfzj/10-years-of-green-bond-issuance-at-eib.

Financial Stability, Financial Services and Capital Markets Union. 2018a. “Final Report of the High-Level Expert Group on Sustainable Finance. European Commission.” Available from https://ec.europa.eu/info/publications/180131-sustainable-finance-report_fr.

Financial Stability, Financial Services and Capital Markets Union. 2018b. “Commission Announces Members of the Technical Expert Group on Sustainable Finance.” European Commission. Available from https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/180613-sustainable-finance-press-release_en.pdf.

Financial Stability, Financial Services and Capital Markets Union. 2019. Technical expert group on sustainable finance (TEG). Available from https://ec.europa.eu/info/publications/sustainable-finance-technical-expert-group_en.

Gould, Rick. 2018. “The Secret to Unlocking Green Finance.” ISOfocus. International Organization for Standardization. Available from https://www.iso.org/news/ref2287.html.

Hachenberg, Britta, and Dirk Schiereck. 2018. “Are Green Bonds Priced Differently from Conventional Bonds?” Journal of Asset Management 19(6): 371–83. Palgrave Macmillan, UK. Available from https://doi.org/10.1057/s41260-018-0088-5.

House, Katie. 2017. “TWG Process Diagram.” Climate Bonds Initiative.

Influence Map. 2019. “Lobbying and Corporate Influence.” Available from https://influencemap.org/page/About-Us.

Kapraun, Julia, and Christopher Scheins. 2019. “(In)-Credibly Green: Which Bonds Trade at a Green Bond Premium?” Proceedings of Paris December 2019 Finance Meeting EUROFIDAI–ESSEC. Available from SSRN 3347337.

Karpf, Andreas, and Antoine Mandel. 2018. “The Changing Value of the ‘Green’ Label on the US Municipal Bond Market.” Nature Climate Change 8:161–65.

Kidney, Sean. 2009. “Climate Bonds Launch: Fast-Track Solution to Low-Carbon Economy.” CBI. Available from https://www.climatebonds.net/2014/05/climate-bonds-launch-fast-track-solution-low-carbon-economy.

Kidney, Sean. 2013. “FYI: full text of Green Bonds Framework—steering c’ttee now set up w. BoAML, Citi, JPM, MS +others in process of joining.” Climate Bonds Initiative. Available from https://www.climatebonds.net/2014/05/fyi-full-text-green-bonds-framework-steering-cttee-now-set-w-boaml-citi-jpm-ms-others.

Kidney, Sean, Karl Mallon, Nick Silver, and Cynthia Williams. 2009. “Financing a

Rapid, Global Transition to a Low-Carbon Economy. CBI. Available from https://www.climatebonds.net/files/uploads/2012/12/climate_bonds_28Dec09.pdf.

Larcker, David F., and Edward M Watts. 2020. “Where’s the Greenium?” Rock Center for Corporate Governance at Stanford University Working Paper No. 239; Stanford University Graduate School of Business Research Paper No. 19-14; Journal of Accounting and Economics 69(2–3). Available from https://doi.org/10.1016/j.jacceco.2020.101312.

Lazarova, Iliana. 2016. “Welcome to the Wild West of Green Bonds.” Available from https://www.greenbiz.com/article/welcome-wild-west-green-bonds?utm_source=Sailthru&utm_medium=email&utm_campaign=Issue:%202016-03-10%20Utility%20Dive%20Newsletter%20[issue:5197]&utm_term=Utility%20%20Dive.

Leigh-Bell, Justine. 2015. “Climate Bonds Releases Standards V2.0.” Institutional Asset Manager, December 23, 2015. Global Fund Media. Available from https://www.institutionalassetmanager.co.uk/2015/12/23/235069/climate-bonds-releases-standards-v20.

Linnenluecke, Martina K., Tom Smith, and Brent McKnight. 2016. “Environmental Finance: A Research Agenda for Interdisciplinary Finance Research.” Economic Modelling, 59:124–30.

Lovell, Heather. 2013. “Climate Change, Markets and Standards: The Case of Financial Accounting.” Economy and Society. 43(2): 260–284.

Lovell, Heather. 2015. The Making of Low Carbon Economies. London: Routledge.

MacKenzie, Donald. 2008. “Making Things the Same: Gases, Emission Rights and the Politics of Carbon Markets. Accounting, Organizations and Society 34:440–455.

McDermott, Constance, Emily Noah, and Benjamin Cashore. 2008. “Differences that ‘Matter’? A Framework for Comparing Environmental Certification Standards and Government Policies.” Journal of Environmental Policy and Planning 10, no. 1 (March): 47–70.

Partridge, Candace, and Francesca Romana Medda. 2020. “The Evolution of Pricing Performance of Green Municipal Bonds.” Journal of Sustainable Finance & Investment, 10:44–64. Available from https://doi.org/10.1080/20430795.2019.1661187.

Pell, Elza Holmstedt. 2013. “Climate Bonds Initiative Launches Solar Bond Standards.” Environmental Finance. Available from https://www.environmental-finance.com/content/news/climate-bonds-initiative-launches-solar-bond-standards.html. Accessed 27 May 2020.

Petheram, Rhys. 2017. “Views On: The Standards for Green Bonds.” Jupiter Asset Management: Insights. Available from https://www.jupiteram.com/UK/en/Professional-Investors/Insights/Rhys-Petheram/Rhys-Petheram-Views-on-the-standards-for-green-bonds.

Riles, Annelise. 2011. Collateral Knowledge: Legal Reasoning in the Global Financial Markets. Chicago: University of Chicago Press.

Silver, Nick. 2017. Finance, Society and Sustainability: How to Make the Financial System Work for the Economy, People and Planet (Springer).

Technical Expert Group on Sustainable Finance Subgroup: Taxonomy. 2019. “Progress Report.” European Commission. Available from https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/sustainable-finance-teg-subgroup-taxonomy-progress-report_en.pdf.

Tripathy, Aneil. 2017. “Translating to Risk: The Legibility of Climate Change and Nature in the Green Bond Market.” Economic Anthropology 4:239–50.

Wood, David, and Katie Grace. 2011. “A Brief Note on the Global Green Bond Market.” IRI Working Paper. Initiative for Responsible Investment (IRI) and the Hauser Center for Nonprofit Organizations, both at Harvard University.

Wulandari, Febi, Dorothea Schäfer, Andreas Stephan, and Chen Sun. 2018. “The Impact of Liquidity Risk on the Yield Spread of Green Bonds.” Finance Research Letters 27:53–59.

Xu, Nan, and Wang Yao. 2016. “China’s Green Bond Market Booms with More Clarity in Policy.” China Dialogue, July 29, 2016. Available from https://www.chinadialogue.net/article/show/single/en/9128-China-s-green-bond-market-booms-with-more-clarity-in-policy.

Zerbib, Olivier David. 2019. “The Effect of Pro-Environmental Preferences on Bond Prices: Evidence from Green Bonds.” Journal of Banking & Finance 98:39–60.